When the US Economy Looks Great, Why Bother Going Global?

It’s a fair question. The US unemployment rate sits at 4.3%, and real GDP clocked in at $24,152.66 billion — a massive economic engine by any measure. When things look this good at home, buying stocks in other countries can feel unnecessary, even risky.

But a strong US economy today doesn’t tell you which stock market will outperform over the next 10 or 20 years. History has shown, repeatedly, that leadership rotates between US and international markets in ways that are nearly impossible to predict ahead of time. That’s exactly why the diversification question deserves a careful, checklist-style look — not a gut-feel answer.

This article walks you through a practical checklist to help you decide whether adding VXUS (Vanguard Total International Stock ETF) or VT (Vanguard Total World Stock ETF) makes sense for your portfolio right now.

What Are VXUS and VT, Exactly?

Before we get to the checklist, here’s a quick rundown of what these two funds actually are.

VXUS tracks the FTSE Global All Cap ex US Index, meaning it owns essentially every investable stock outside the United States — developed markets like Canada, Europe, and Japan, plus emerging markets including China and India (source). The fund holds thousands of positions, so even its largest single holding barely registers as a concentration risk (source). VXUS also pays a meaningful dividend yield, which adds an income component on top of any price appreciation (source). Its expense ratio is 0.08%, and its most recent closing price was $83.03.

VT is the Vanguard Total World Stock ETF. It bundles US and international stocks into a single fund, giving you global exposure in one ticker. VT’s expense ratio is 0.07%, and its most recent closing price was $153.68.

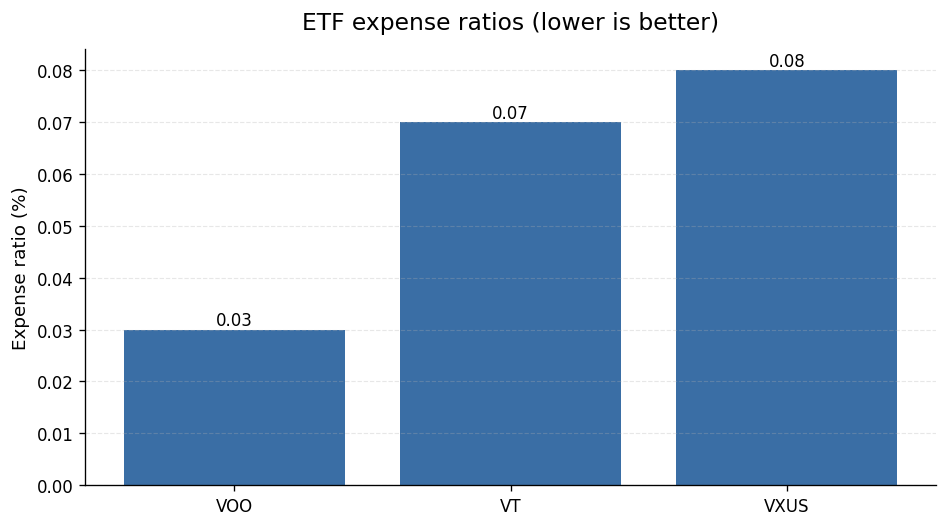

For comparison, a US-only fund like VOO (the Vanguard S&P 500 ETF) carries an expense ratio of 0.03%. So adding international exposure via VXUS or VT does cost a bit more — though all three are still extraordinarily cheap by industry standards.

Why the Strong US Economy Isn’t the Whole Story

A strong economy and a strong stock market are related — but they’re not the same thing. Stock prices reflect expectations about the future, not just current conditions. By the time unemployment is low and GDP is humming, much of that good news is often already baked into stock prices.

Some of the most compelling periods for international stocks have come precisely when the US economy was running hot and US valuations were stretched. US companies have held durable advantages in earnings growth and capital returns that international markets haven’t always matched (source) — but that gap doesn’t stay constant, and it doesn’t last forever.

The case for owning some international exposure isn’t that international stocks will definitely beat the US. It’s that you can’t know in advance which will win, and diversification is the time-tested way to avoid being wrong in a costly way.

Your 8-Point Checklist: Should You Add VXUS or VT?

Work through each item honestly. There are no right or wrong answers — just honest ones.

✅ 1. Is Your Portfolio Currently 100% US Stocks?

If every dollar you own in equities is in US-focused funds, you have a geographic concentration risk. A portfolio concentrated entirely in US equities carries its own set of risks (source). That doesn’t mean you need to rush out and buy international stocks today, but you should at least make that choice consciously — not by default.

If yes: International funds like VXUS or VT are worth considering.

If no: Think about what percentage is already international and whether it fits your goals.

✅ 2. Is Your Time Horizon 10 Years or Longer?

International stocks have underperformed domestic stocks over long stretches (source). But over very long periods, diversification tends to smooth out the rough patches. If you’re investing for retirement decades away, you have time to ride out stretches when international lags.

If your time horizon is shorter — say, under five years — the added volatility of international exposure, including currency swings, may not be worth it.

If 10+ years: International diversification makes more sense.

If under 5 years: Proceed carefully and think hard about whether you can stomach the extra volatility.

✅ 3. Do You Understand Currency Risk?

When you own international stocks, you’re also exposed to foreign currencies. When the US dollar strengthens, international returns shrink in dollar terms — even if foreign stocks are rising in their local currencies (source). Both VXUS and VT carry this unhedged exposure.

That’s not necessarily a bad thing — currency moves can work in your favor, too. But you should know it comes with the territory.

If you understand and accept currency risk: Check this box.

If currency risk makes you uncomfortable: A smaller allocation might let you sleep at night.

✅ 4. Are You Chasing Recent Performance — or Making a Strategic Decision?

This one matters a lot. International stocks have had a strong run recently (source), and it’s tempting to jump in after a big move. But the valuation argument for international stocks has been compelling for most of the past decade — and it hasn’t always translated into outperformance (source).

If you’re adding VXUS or VT because international diversification fits your long-term plan, that’s a solid reason. If you’re adding it purely because it’s been hot lately, that’s a warning sign.

If strategic: Great reason to add international exposure.

If chasing performance: Pause and reconsider.

✅ 5. Can You Handle Lumpy or Inconsistent Income?

VXUS pays dividends, which is a nice bonus. But the payments aren’t evenly distributed throughout the year — the timing and size of distributions can vary significantly from quarter to quarter (source). If you’re counting on steady quarterly income from your portfolio, that inconsistency could get frustrating.

If income consistency matters to you: Factor this into your decision.

If you’re a long-term accumulator: Dividend timing matters less — you’re reinvesting anyway.

✅ 6. Do You Prefer Simplicity? (VT Might Be Your Answer)

If managing separate US and international funds sounds like more complexity than you want, VT solves that problem neatly. At 0.07% per year, you get a single fund that owns both US and international stocks in one package, automatically rebalanced to global market weights.

The tradeoff is that VT costs slightly more than a pure US fund like VOO at 0.03%, and you give up the ability to customize your US-to-international split.

If you want simplicity: VT is a strong candidate.

If you want control over your allocation: A combination of a US fund plus VXUS at 0.08% gives you more flexibility.

✅ 7. Are You Comfortable With Emerging-Market Exposure?

Both VXUS and VT include emerging markets — countries like China, India, Brazil, and others. These markets can be more volatile than developed markets, and they carry additional risks including political instability and less regulatory transparency.

Emerging markets make up a meaningful slice of VXUS’s holdings (source). Worth knowing before you buy.

If you’re comfortable with emerging-market risk: VXUS or VT works.

If you want developed-market-only international exposure: Look into a developed-market-only fund instead.

✅ 8. Does the Extra Cost Fit Your Plan?

All three of these funds are cheap. But cost differences compound over time. VOO charges 0.03% per year. VT charges 0.07%. VXUS charges 0.08%. On a $100,000 portfolio, the difference between VOO and VXUS is about $50 per year — genuinely small, but worth acknowledging.

If the small cost difference fits your budget: International funds remain highly cost-efficient.

If you’re extremely cost-sensitive: VOO or a similar US-only fund keeps fees at rock bottom.

What the US Economic Data Actually Tells Us (and What It Doesn’t)

Let’s bring the macro picture back in. The US unemployment rate is 4.3% — a level that signals a healthy labor market. Real GDP stands at $24,152.66 billion, reflecting an enormous and productive economy. And nominal US GDP reached approximately $28.75 trillion as of the most recent World Bank reading, with GDP per capita at roughly $84,534.

Those are genuinely impressive numbers. The US is a large, productive, and innovative economy. But here’s what those numbers don’t tell you:

- They don’t tell you whether US stocks are fairly valued right now.

- They don’t tell you whether international stocks are undervalued relative to the US.

- They don’t tell you what earnings growth will look like in Germany, Japan, or India over the next decade.

Strong economic fundamentals are a reason to feel good about your US holdings. They’re not a reason to ignore the rest of the world’s investable markets.

VXUS vs. VT: Which One If You Decide to Add International?

If you work through the checklist and decide international exposure fits your plan, the next question is which fund.

Choose VXUS if:

– You already own a US equity fund and want to add international on top of it.

– You want to set your own US-to-international ratio.

– You’re comfortable with a slightly higher expense ratio of 0.08%.

Choose VT if:

– You want one fund that does everything.

– You’d rather not think about rebalancing between US and international.

– You’re happy to let global market weights determine your allocation.

– You’re comfortable with VT’s expense ratio of 0.07%.

Both are solid, low-cost choices. The right answer depends on how much control you want over your allocation and how much you value simplicity.

The Bottom Line

A strong US economy — low unemployment, robust GDP — is genuinely good news. But it’s not a reason to tune out the rest of the world’s stock markets. International diversification is about acknowledging uncertainty, not abandoning confidence in the US.

If you checked most of the boxes above — long time horizon, understanding of currency risk, a strategic rather than performance-chasing motivation, and comfort with some volatility — then adding VXUS or VT to your portfolio is a reasonable, well-grounded decision. If you checked fewer boxes, there’s no shame in sticking with what you have and revisiting the question later.

The goal isn’t to predict which market wins. The goal is to build a portfolio you can hold through good times and bad — and international diversification has historically helped investors do exactly that.

This article was researched using official U.S. data sources cited inline and reviewed for accuracy before publishing. It is general information, not personalized financial advice. For decisions specific to your situation, consult a licensed professional.

Data refreshed: 2026-06-08. Editorial accuracy verified for cited sources only.

Related reads

- How Inflation in 2025–2026 Affects Your Index Fund Returns Over Time

- VTI vs SCHB vs SPLG: Which Total Market ETF Costs Less for a Roth IRA in 2026?

- CD Ladder Strategy for 2026: How to Use Treasury Rates as Your Benchmark

Armin Cole has been personally investing in index funds and ETFs

for over three years. He started Nestvestify to document what he’s

learning and make data-backed personal finance accessible to everyday

readers — without the jargon. All articles are grounded in official

U.S. data sources including the Federal Reserve (FRED), SEC filings,

and the Bureau of Labor Statistics.