The Dollar Question Every Index Fund Investor Is Asking

If you follow financial news at all, you’ve probably noticed a recurring theme in 2026: international stocks are back in the conversation. After years of US equities dominating the headlines, investors are asking a very reasonable question — does it make sense to add international exposure to a portfolio when the US dollar is strong?

The short answer is: it depends on your time horizon, your current allocation, and how you think about diversification. The longer answer is what this article is for.

We’ll walk through what the currency dynamic actually means for your returns, what the data and expert commentary say about international stocks right now, and how to think practically about funds like VXUS and VT alongside your core US holdings.

Why the Dollar Matters for International Investing

When you invest in international stocks as a US investor, you’re not just betting on foreign companies — you’re also taking on currency exposure. Here’s the basic mechanic: if you own shares of a German company and the euro rises against the dollar, your investment is worth more in dollar terms when you sell, even if the stock price didn’t move. The reverse is also true. When the dollar is strong, foreign-currency profits translate into fewer dollars when they come back to you.

That’s why currency direction matters so much in the international investing decision. As one market strategist noted, the direction of the dollar is “such a key piece of that equation” when evaluating international stocks (source).

A strong dollar creates a natural headwind for US investors holding international stocks — at least in the short run. But short-run headwinds don’t necessarily make international stocks a bad long-term bet.

What Experts Are Saying About International Stocks in 2026

Demand Has Been Strong, but Investors Are Getting More Selective

According to iShares, demand for international stocks in 2026 has been strong. But investors are increasingly becoming more selective in their global exposures, balancing structural conviction with a more cautious near-term backdrop (source). Rather than simply buying broad international funds and walking away, many market participants are seeking more tailored and targeted opportunities within the broad asset class of international equities (source).

iShares notes its own preference for emerging markets over developed economies in 2026, citing factors like AI supply chain exposure and relatively attractive valuations (source). South Korea, for example, is highlighted for its central role in AI infrastructure and semiconductor manufacturing (source).

Valuations: Non-US Stocks Still Trade at a Discount

One of the most frequently cited reasons to consider international exposure is valuation. Even after international stocks outpaced US markets by a wide margin in 2025, non-US stocks generally still trade at significant discounts to their US counterparts (source). For investors who believe in mean reversion over long periods, that gap is hard to ignore.

Fidelity’s 2026 outlook also points to several structural tailwinds: potential opportunities in the global AI supply chain, Europe’s renewed infrastructure and defense spending, and corporate restructuring efforts in Japan (source).

Nearly Every Investor Could Benefit From Some International Exposure

Kristy Akullian, head of iShares investment strategy for the Americas at BlackRock, told CNBC: “Nearly every investor that we speak to could probably benefit from adding some international allocations” (source). Her reasoning is straightforward: most US investors are significantly overweight domestic equities — not just a little overweight relative to a broad benchmark, but “orders of magnitude more overweight” (source).

Put simply, if your portfolio is 100% US stocks, you’re making a very concentrated bet on one country’s market, regardless of how that country has performed recently.

The Diversification Argument Doesn’t Disappear When the Dollar Is Strong

Here’s the key insight that gets lost in the dollar-strength conversation: diversification isn’t primarily about maximizing short-term returns. It’s about smoothing out your ride over time and making sure one part of your portfolio is always working even when another part is struggling (source).

A strong dollar may compress your near-term returns from international holdings. But over a full market cycle — which can span a decade or more — currency effects tend to be less dominant than the underlying performance of the businesses you own. Fidelity notes that short-term performance is never guaranteed, but international stocks can provide valuable diversification benefits when added to a portfolio of US stocks (source).

The practical takeaway: if you’re a long-term investor with a 20- or 30-year horizon, waiting for the “perfect” currency environment to add international exposure means you may never add it at all.

The Funds: Your Main Options for International Exposure

If you decide international stocks make sense for your portfolio, here are the most commonly used low-cost index ETFs to consider. All expense ratios below come from Vanguard’s official fund profile pages.

VT — Vanguard Total World Stock ETF

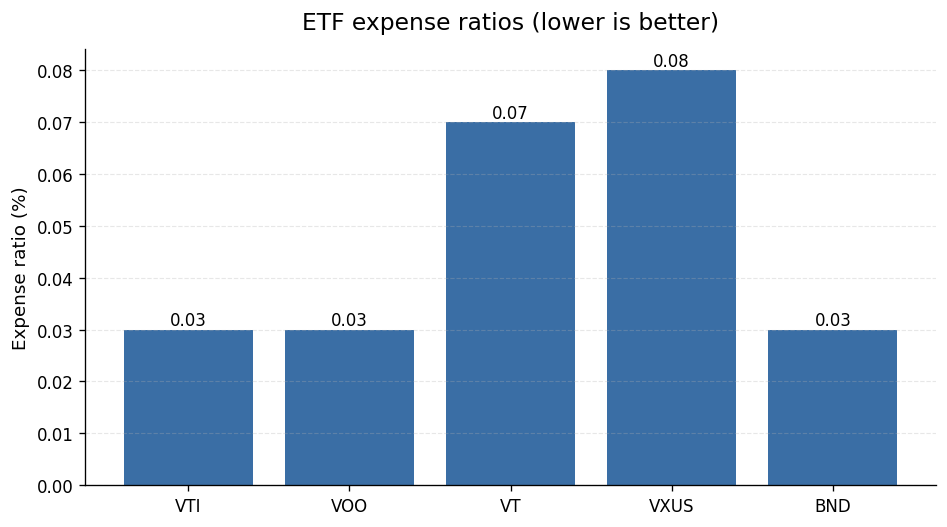

VT is the all-in-one option. It holds both US and international stocks in a single fund. Its expense ratio is 0.07% (source). If you want global diversification without managing two separate funds, VT is the simplest path. The tradeoff is that you give up some control over your exact US-to-international split.

VXUS — Vanguard Total International Stock ETF

VXUS is the dedicated international sleeve. It holds stocks from developed and emerging markets outside the US. Its expense ratio is 0.08% (source). Pairing VXUS with a US fund like VTI gives you more flexibility to dial in your exact allocation — say, 80% US and 20% international — and rebalance it over time.

VTI — Vanguard Total Stock Market ETF

VTI is the US-only counterpart, covering the entire US stock market. Its expense ratio is 0.03% (source), and it closed most recently at $363.67 (source). Many investors use a VTI + VXUS combination as the equity core of a simple portfolio.

VOO — Vanguard S&P 500 ETF

VOO tracks the S&P 500, which closed most recently at 7,386.65 (source). VOO’s expense ratio is also 0.03% (source), and it closed most recently at $677.70 (source). Some investors prefer VOO over VTI for their US core and then add VXUS on top for international exposure.

BND — Vanguard Total Bond Market ETF

If you’re building a full three-fund portfolio, BND is the bond component. Its expense ratio is 0.03% (source). Bonds are outside the main scope of this article, but they’re worth mentioning for completeness.

How to Think About Allocation When the Dollar Is Strong

Don’t Try to Time the Currency

Currency forecasting is notoriously difficult, even for professionals. A strong dollar today doesn’t mean a strong dollar in three years. Building your allocation around a currency view is essentially market timing — and most individual investors don’t have an edge there.

A better framework: decide on a target international allocation that reflects your long-term goals and risk tolerance, then stick to it through currency cycles. Dollar strong? You’re buying international stocks at a relative discount in dollar terms. Dollar weak? Your international holdings get a tailwind. Over time, these effects tend to average out.

Consider Your Existing Exposure

Before adding international funds, check what you already own. Many US large-cap companies — the kind that dominate VTI and VOO — derive a significant portion of their revenue from outside the US. That gives you some implicit international exposure even in a US-only fund. It’s not the same as owning foreign-listed companies, but it’s worth acknowledging.

A Common Starting Point

Many financial educators and target-date fund designers use something in the range of 20% to 40% of the equity portion in international stocks as a reasonable baseline. That said, there’s no single correct answer. The right allocation is the one you can stick with through volatility — including stretches when international stocks lag US stocks for years at a time.

Rebalancing Is Your Friend

If you add international exposure, commit to a rebalancing schedule — annually or when your allocation drifts by more than a set percentage. Rebalancing forces you to buy low and sell high in a systematic way, without relying on gut feelings about which region will win next year.

The Bottom Line: Strong Dollar, Long Horizon

A strong US dollar creates a genuine short-term headwind for international stocks held by US investors. That’s real, and it’s worth understanding. But it’s not a reason to abandon the diversification case entirely.

The structural arguments for holding some international exposure — lower valuations relative to US stocks, diversification benefits, and exposure to growth in emerging economies — don’t evaporate just because the dollar is strong today. And as iShares notes, demand for international stocks in 2026 has been strong even in this environment, with investors becoming more selective rather than retreating entirely (source).

If you’re a long-term index fund investor who is currently 100% in US equities, the question isn’t really “is now the perfect time to add international stocks?” The better question is: “Does my portfolio reflect my actual beliefs about long-term diversification?” For most people, the honest answer is that some international exposure makes sense — and the cost of entry is lower than ever, with funds like VXUS at 0.08% (source) and VT at 0.07% (source) per year.

The dollar will have its cycles. Your retirement timeline is longer than any of them.

This article was researched using official U.S. data sources cited inline and reviewed for accuracy before publishing. It is general information, not personalized financial advice. For decisions specific to your situation, consult a licensed professional.

Data refreshed: 2026-06-10. Editorial accuracy verified for cited sources only.

Related reads

- Strong US Economy in 2026: Should You Still Add VXUS or VT to Your Portfolio?

- Fidelity ZERO Funds vs Vanguard VTI: Is a 0% Expense Ratio Actually Better for Index Investors?

- How Inflation in 2025–2026 Affects Your Index Fund Returns Over Time

Armin Cole has been personally investing in index funds and ETFs

for over three years. He started Nestvestify to document what he’s

learning and make data-backed personal finance accessible to everyday

readers — without the jargon. All articles are grounded in official

U.S. data sources including the Federal Reserve (FRED), SEC filings,

and the Bureau of Labor Statistics.