Why Choosing the Right Roth IRA Broker Still Matters in 2026

All three of the biggest names in retail investing — Fidelity, Schwab, and Vanguard — now charge $0 to buy or sell stocks and ETFs online (source). So if commissions are off the table, what actually separates them for a Roth IRA investor?

More than you might expect. Fund expense ratios, cash sweep yields, robo-advisor fees, mutual fund minimums, branch access, and customer service all differ in ways that add up to real dollars over a 20- or 30-year retirement timeline. This guide breaks it all down so you can pick the right home for your Roth IRA — or confirm that the one you already have is working for you.

The One Thing They All Share: $0 Commissions and $0 Account Minimums

Start with the good news. All three brokerages charge $0 for online stock and ETF trades (source), and none require a minimum deposit to open an account (source). You can open a Roth IRA with any of them today with whatever you have — even just a few dollars.

All three also support every major IRA account type: Traditional IRA, Roth IRA, SEP IRA, and more (source). And all three are SIPC members, which provides a baseline layer of investor protection (source).

For 2025, the IRS sets the annual Roth IRA contribution limit at $7,000 (source). If you’re 50 or older, a $1,000 catch-up contribution brings that total to $8,000 (source).

Where They Differ: The Details That Actually Matter

Expense Ratios: Fidelity’s Zero Funds vs. Vanguard’s Near-Zero ETFs

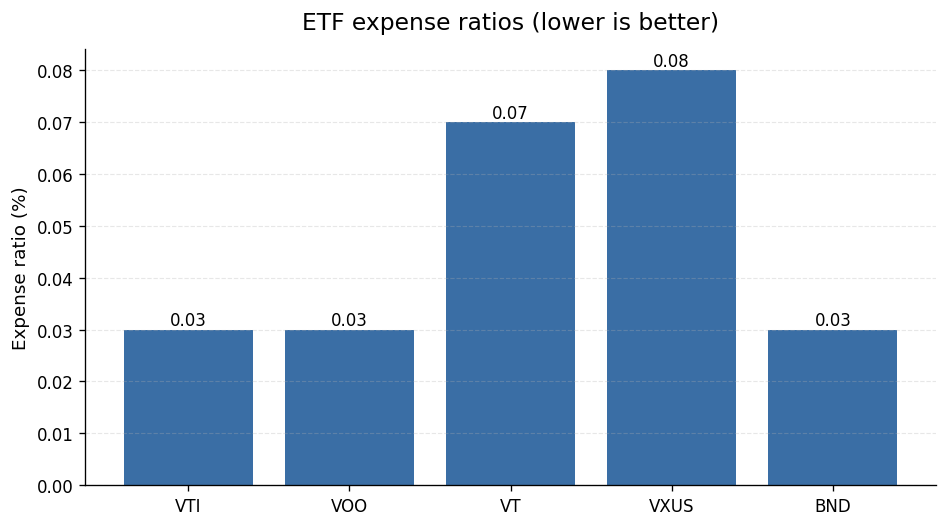

This is where the most meaningful cost difference lives. Vanguard pioneered the low-cost index fund and still offers some of the cheapest ETFs on the market:

- VTI (Vanguard Total Stock Market ETF): 0.03% expense ratio (source)

- VOO (Vanguard S&P 500 ETF): 0.03% (source)

- BND (Vanguard Total Bond Market ETF): 0.03% (source)

- VXUS (Vanguard Total International Stock ETF): 0.08% (source)

- VT (Vanguard Total World Stock ETF): 0.07% (source)

Those are genuinely tiny numbers. But Fidelity goes one step further with its proprietary ZERO funds, which carry a 0.00% expense ratio — literally free to hold (source). The catch: FZROX and its siblings are exclusive to Fidelity. You can’t transfer them in-kind to another broker. Vanguard ETFs like VTI, by contrast, are portable — you can hold them at Fidelity, Schwab, or Vanguard itself.

For most long-term Roth IRA investors, the gap between 0.00% and 0.03% is negligible in absolute dollars. The bigger takeaway is that all three brokerages give you access to extremely low-cost index investing.

Mutual Fund Minimums: Vanguard Has a Higher Bar

If you prefer mutual funds over ETFs, Vanguard’s minimums are worth knowing. Vanguard requires a minimum investment of $1,000–$3,000 for its index mutual funds (source). Fidelity and Schwab, by contrast, have no minimums on most of their index mutual funds (source).

For new investors just starting a Roth IRA, that’s a real practical difference. If you’re contributing a small amount each month and want to use mutual funds, Fidelity or Schwab will give you more flexibility. If you’re at Vanguard and below the mutual fund minimums, you can always buy the ETF version — VTI instead of VTSAX, for example — with no minimum at all.

Cash Sweep Yields: Where Your Uninvested Money Lives

Here’s a feature most people overlook: what happens to the cash sitting in your account while you decide what to buy? Each broker handles this differently (source).

Fidelity and Vanguard automatically sweep idle cash into money market funds, which tend to offer more competitive yields. Schwab defaults to a lower-yield bank sweep — meaning uninvested cash earns less unless you manually move it to a money market fund (source). For a Roth IRA where you’re making regular contributions and buying periodically, this matters most when cash is sitting between purchases.

Robo-Advisors: Free vs. Paid

All three offer automated investing options, but the costs vary:

- Fidelity Go: $0 advisory fee, no minimum balance required (source)

- Schwab Intelligent Portfolios: $0 advisory fee (source)

- Vanguard Digital Advisor: charges approximately 0.20% per year (source)

If you want a hands-off approach for your Roth IRA and don’t want to pay for it, Fidelity Go stands out — $0 fees and no minimum balance requirement. Schwab’s robo-advisor is also free but requires a higher starting balance (source).

Branch Access and Customer Service

Not everyone wants to handle everything online, and this is where the three brokers diverge most visibly:

- Fidelity: Has investor centers across the country and offers 24/7 customer service (source)

- Schwab: Has the most physical branch locations of the three, making it a strong pick for investors who value in-person help (source)

- Vanguard: Operates entirely online — no physical branches (source)

If you ever want to walk into a branch and talk to someone face-to-face, Vanguard simply isn’t an option. Fidelity and Schwab both fill that gap, with Schwab holding the edge in sheer branch count.

Banking Integration

Schwab stands out here. It offers a full banking suite — checking, savings, and debit card — alongside its brokerage and IRA accounts (source). Fidelity offers a cash management account with a debit card and ATM rebates, though it’s not a full bank (source). Vanguard’s banking features are minimal (source). If you want your investing and day-to-day banking under one roof, Schwab has the most complete setup.

Trading Platforms and Research

For most Roth IRA investors who are buying and holding index funds, the trading platform barely matters. But if you’re also an active investor or want deeper research tools:

- Fidelity offers Active Trader Pro and is rated highly for research quality (source)

- Schwab offers thinkorswim, widely regarded as one of the best platforms for active traders (source)

- Vanguard has a basic web portal suited for buy-and-hold investors (source)

Fractional Shares

All three now offer fractional share investing, but with different scopes. Fidelity and Schwab allow fractional purchases on a broad range of stocks and ETFs (source). Vanguard limits fractional shares to Vanguard ETFs only — so you can buy a fraction of VTI, but not a fraction of a third-party ETF (source).

Ownership Structure: Vanguard Is Different by Design

Vanguard has a unique ownership structure: it is client-owned, meaning investors in its funds effectively own the company (source). Fidelity is a private for-profit company, and Schwab is publicly traded (source). Vanguard’s structure aligns its incentives directly with keeping costs low — there are no outside shareholders to pay. That philosophy is a big part of why its expense ratios are so competitive.

Head-to-Head Summary: Which Broker Wins for Your Roth IRA?

| Feature | Fidelity | Schwab | Vanguard |

|---|---|---|---|

| Stock/ETF commissions | $0 | $0 | $0 |

| Account minimum | $0 | $0 | $0 |

| Cheapest index fund ER | 0.00% (FZROX) | ~0.03% | 0.03% (VTI/VOO/BND) |

| Mutual fund minimums | $0 | $0–$100 | $1,000–$3,000 |

| Robo-advisor fee | $0 | $0 | ~0.20%/yr |

| Fractional shares | Broad | Broad | Vanguard ETFs only |

| Physical branches | Yes | Yes (most of the three) | None |

| 24/7 customer service | Yes | Yes | No |

| Banking integration | Limited | Full | Minimal |

| Cash sweep default | Competitive | Lower yield | Competitive |

Who Should Pick Which Broker?

Choose Fidelity if…

You’re opening your first Roth IRA, want the most features for free, value 24/7 customer service, and want access to both zero-expense-ratio funds and a no-minimum robo-advisor. Fidelity is the most versatile all-around pick for most investors (source).

Choose Schwab if…

You want banking and investing under one roof, prefer the most branch locations of the three, or are an active trader who wants access to thinkorswim alongside your retirement accounts (source). Schwab’s full banking suite is genuinely useful if you want one institution handling everything.

Choose Vanguard if…

You’re a committed buy-and-hold index investor who values the client-owned structure and is already invested in Vanguard funds. If you have a working setup at Vanguard, there’s generally no reason to disrupt it (source). For new accounts, Fidelity and Schwab offer more features at the same or lower cost.

Don’t Forget Your Contribution Limits

No matter which broker you choose, the IRS caps how much you can put into a Roth IRA each year. For tax year 2025, the limit is $7,000 (source). If you’re 50 or older, the catch-up contribution adds another $1,000 (source), bringing the total to $8,000. Income limits also apply to Roth IRA eligibility — check IRS guidance for the current phase-out ranges.

The Bottom Line

The commission wars are over — you won. All three brokers charge $0 to trade ETFs online (source), and none require a minimum to open a Roth IRA (source). The real differentiators are the expense ratios on the funds you hold, what happens to your idle cash, whether you want a free robo-advisor, and how much in-person support you need.

For most new Roth IRA investors, Fidelity edges out the competition on features and flexibility. Schwab is the better choice if banking integration or branch access is a priority. And Vanguard remains an excellent home for anyone already there and committed to its low-cost ETF lineup — VTI at 0.03% (source) and VOO at 0.03% (source) are as cheap as index investing gets outside of Fidelity’s proprietary ZERO funds.

The best broker is the one you’ll actually use consistently. Pick one, open the account, and start contributing.

This article was researched using official U.S. data sources cited inline and reviewed for accuracy before publishing. It is general information, not personalized financial advice. For decisions specific to your situation, consult a licensed professional.

Data refreshed: 2026-05-31. Editorial accuracy verified for cited sources only.

Related reads

- 3-Fund Portfolio Bond Allocation When the 10-Year Treasury Yield Is Above 4%

- Is Your Savings Account Actually Beating Inflation in 2026?

- High-Yield Savings Account Interest Taxes 2026: What You Owe the IRS

Armin Cole has been personally investing in index funds and ETFs

for over three years. He started Nestvestify to document what he’s

learning and make data-backed personal finance accessible to everyday

readers — without the jargon. All articles are grounded in official

U.S. data sources including the Federal Reserve (FRED), SEC filings,

and the Bureau of Labor Statistics.