Why Bond Yields Matter Right Now

If you’ve been putting off thinking about the bond slice of your three-fund portfolio, now is a good time to revisit it. The 10-year Treasury Constant Maturity Rate recently hit 4.5% (source) — a level that hasn’t felt routine in years. That number matters because it’s a rough benchmark for what the bond market will pay you to lend money to the U.S. government for a decade.

When yields are high, bonds become more interesting — not just as a safety net, but as a genuine income-generating piece of a diversified portfolio. So if you’re running a classic three-fund setup, this is a good moment to check whether your bond allocation still fits your goals.

A Quick Refresher on the Three-Fund Portfolio

The three-fund portfolio is a simple, low-cost investing approach that uses diversification to reduce risk. As Financial Samurai explains, diversification works best when the assets involved are inversely correlated — meaning when one drops, the other doesn’t necessarily follow. Harry Markowitz, the Nobel Prize winner widely credited as the founder of Modern Portfolio Theory, showed that combining less-correlated assets can produce stronger returns with less volatility (source).

The three-fund portfolio puts that idea into practice with just a handful of low-cost index funds — typically one domestic stock fund, one international stock fund, and one bond fund. That’s it. No stock-picking, no market timing, no complicated rebalancing formulas.

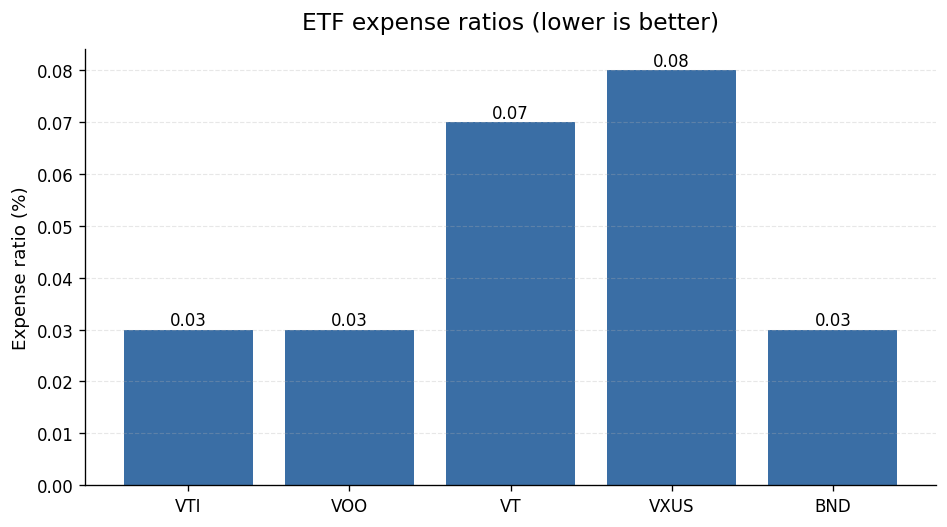

The appeal is largely about cost. Vanguard’s VTI (Total Stock Market ETF) carries an expense ratio of just 0.03% (source), and so does VOO (S&P 500 ETF) at 0.03% (source). On the international side, VT (Total World Stock ETF) comes in at 0.07% (source) and VXUS (Total International Stock ETF) at 0.08% (source). The bond leg, BND (Total Bond Market ETF), also costs just 0.03% (source).

Keeping costs low is one of the most reliable ways to improve long-term returns, and these expense ratios reflect that philosophy.

What Does ‘Bond Allocation’ Actually Mean?

Your bond allocation is simply the percentage of your total portfolio that sits in bonds or a bond fund. If you have $100,000 invested and $20,000 is in BND, your bond allocation is 20%.

The traditional rule of thumb is to hold a bond percentage roughly equal to your age — a 30-year-old holds 30% bonds, a 60-year-old holds 60%. But that rule was designed for a different interest-rate environment, and many investors today use a more aggressive version, such as subtracting their age from 110 or 120 to get their stock percentage, leaving a smaller slice for bonds when they’re young.

There’s no universally correct allocation. What matters is choosing a split you can stick with through both up and down markets — and revisiting it when the interest-rate landscape shifts in a meaningful way.

The Rate Environment Today: What the Numbers Say

Here’s where rates actually stand right now (as of the dates noted in each source):

- 10-Year Treasury yield: 4.5% (FRED DGS10) — The yield on a 10-year U.S. government bond. It’s also the rough hurdle rate for BND, since BND holds a broad mix of U.S. investment-grade bonds with an average duration in that ballpark.

- Federal Funds Effective Rate: 3.64% (FRED FEDFUNDS) — The overnight rate banks charge each other, set by Federal Reserve policy. It anchors the short end of the yield curve.

- Weighted-average yield on outstanding U.S. Treasury Bills: 3.696% (Treasury fiscaldata) — Short-term government paper is yielding close to the fed funds rate, as you’d expect.

- Average yield on outstanding U.S. Series I Savings Bonds: 4.349% (Treasury fiscaldata) — Worth knowing, though I Bonds work differently from a bond fund.

- BND latest close: $73.28 (Alpha Vantage) — The share price of BND itself, useful as a reference if you’re tracking your holdings.

The takeaway: across the yield curve, bonds are paying more than they have in many years. That changes the calculus for how much you might want to hold.

Why a Higher Yield Changes the Bond Allocation Conversation

When bond yields were near zero, the case for a large bond allocation was mostly about stability — bonds cushioned the blow when stocks fell, but they paid almost nothing. At 4.5% on the 10-year Treasury, bonds are pulling double duty: they still provide some buffer against stock-market volatility, and they’re generating real income.

Here’s why that matters for your allocation decisions:

1. Higher Starting Yields Mean Better Long-Term Returns from Bonds

The yield at which you buy a bond — or a bond fund — is the single best predictor of what it will return over its duration. When the 10-year yield is 4.5% (source), a bond fund with a similar average duration is likely to return something in that neighborhood over the next decade, all else equal. That’s a much stronger argument for holding bonds than when yields were sitting near 1% or 2%.

This doesn’t mean bonds are safe in the short run — prices still move inversely with rates, and if yields climb further, BND’s price (currently $73.28 per share, source) could dip. But for a long-term investor, the income stream at today’s yields is genuinely attractive.

2. The Diversification Argument Still Holds

The three-fund portfolio philosophy is built on the idea that including assets with lower correlation to each other smooths out your portfolio’s ride (source). Bond funds and stock funds don’t always move in lockstep, and that difference in behavior is a big part of what makes the three-fund approach so durable over long periods.

3. The Fed Funds Rate Gives Context for Short-Term Bonds

With the federal funds rate at 3.64% (source), the short end of the yield curve is also paying reasonably well. The weighted-average yield on outstanding Treasury bills is 3.696% (source). That’s worth considering if you’re deciding between a total bond market fund — which holds a mix of short, intermediate, and long-term bonds — versus a short-term bond fund or cash equivalent.

How to Think About Your Bond Allocation: A Checklist

Here’s a practical checklist for reviewing your bond allocation in this rate environment:

✅ Step 1: Know Your Time Horizon

If you’re more than 15 years from retirement, a smaller bond allocation — say, 10–20% — may make sense. You have time to ride out stock-market swings, and stocks have historically delivered stronger long-term growth. If you’re within 10 years of retirement, a larger bond allocation (30–50%) can reduce the risk that a market downturn takes a big bite out of your nest egg right when you need it most.

✅ Step 2: Check Your Gut Reaction to Volatility

Risk tolerance isn’t just a number on a questionnaire. It’s how you actually behave when your portfolio drops 20% in a month. If you know from experience that you’ll panic-sell during a downturn, a higher bond allocation might be worth the lower expected return — because it keeps you in the game. A portfolio you can stick with beats a theoretically optimal one you’ll abandon.

✅ Step 3: Decide Between a Total Bond Fund and Shorter-Duration Options

BND holds a broad mix of U.S. investment-grade bonds at a 0.03% expense ratio (source). It’s the default choice for the bond leg of most three-fund portfolios. But with the yield curve relatively flat — the 10-year at 4.5% (source) versus T-bills at 3.696% (source) — you’re not giving up a huge amount of yield by staying shorter. Some investors in this environment prefer a short-term bond fund or even a money market fund for their “safe” allocation, accepting slightly lower yield in exchange for less interest-rate sensitivity.

There’s no wrong answer — it depends on your view of where rates are headed and how much price fluctuation you can stomach in the bond portion of your portfolio.

✅ Step 4: Keep Costs in Check

One of the biggest advantages of the three-fund approach is that every fund in the lineup is extremely cheap. BND’s 0.03% expense ratio (source) means you’re keeping almost every dollar of yield the fund generates. Compare that to actively managed bond funds, which can charge significantly more — every extra basis point in fees is a direct hit to your net return.

✅ Step 5: Rebalance Thoughtfully

Once you set your target allocation, stick to it with periodic rebalancing — but don’t overdo it. Once or twice a year is typically enough for most investors. In tax-advantaged accounts like a 401(k) or IRA, rebalancing is simpler because you don’t have to worry about triggering a taxable event. In a taxable brokerage account, consider directing new contributions toward whichever fund has drifted below its target weight before you sell anything.

✅ Step 6: Don’t Let Yield-Chasing Distort Your Allocation

Yes, the 10-year Treasury yield is 4.5% (source) — but that’s not a reason to pile everything into bonds. Stocks still offer growth potential that bonds generally don’t. The whole point of the three-fund approach is balance. Use the attractive yields as a reason to feel good about your bond allocation, not as a reason to gut your stock allocation.

Sample Allocations at Different Life Stages

Here are three rough examples to make this concrete. These are illustrations, not personalized advice:

Early career (20s–30s): 80–90% stocks (split between domestic and international), 10–20% bonds. At this stage, time is your biggest asset. A small bond allocation provides a bit of ballast without dragging down long-term growth.

Mid-career (40s–50s): 60–70% stocks, 30–40% bonds. You’re starting to think more seriously about protecting what you’ve built. A larger bond allocation reduces the damage from a bad sequence of returns as you approach retirement.

Near or in retirement (60s+): 40–60% stocks, 40–60% bonds. Preserving capital and generating income take center stage. At 4.5% on the 10-year (source), bonds are doing meaningful work in this part of the portfolio.

These are starting points. Your actual allocation should reflect your full financial picture — income, expenses, other assets, Social Security timing, and more.

The Bottom Line

The three-fund portfolio works because it’s simple, low-cost, and diversified. With the 10-year Treasury yield at 4.5% (source) and the federal funds rate at 3.64% (source), the bond leg of your portfolio is doing real work right now — not just acting as a placeholder. BND, at a 0.03% expense ratio (source) and a recent price of $73.28 per share (source), remains the go-to choice for most three-fund investors.

The checklist above isn’t about timing the market — it’s about making sure your allocation reflects your actual goals, time horizon, and risk tolerance. Run through it once a year, adjust if your life circumstances change, and let the market do the rest.

This article was researched using official U.S. data sources cited inline and reviewed for accuracy before publishing. It is general information, not personalized financial advice. For decisions specific to your situation, consult a licensed professional.

Data refreshed: 2026-05-29. Editorial accuracy verified for cited sources only.

Related reads

- High-Yield Savings Account Interest Taxes 2026: What You Owe the IRS

- Openbank High-Yield Savings Account Review: Is It Worth It?

- 9-Month CD vs. High-Yield Savings Account: Which Is Better for Your Money in 2026?

Armin Cole has been personally investing in index funds and ETFs

for over three years. He started Nestvestify to document what he’s

learning and make data-backed personal finance accessible to everyday

readers — without the jargon. All articles are grounded in official

U.S. data sources including the Federal Reserve (FRED), SEC filings,

and the Bureau of Labor Statistics.