The Savings Rate Is Telling Us Something Important

If you’ve felt like money has been slipping through your fingers lately, you’re not imagining it. The U.S. personal savings rate — the share of after-tax income that Americans actually set aside — sits at just 2.6% as of April 2026. That’s a razor-thin margin, and it has real consequences for one of the most important financial safety nets you can build: your emergency fund.

Below, we’ll break down what that savings rate number really means, look at where Americans actually stand with their emergency savings today, and give you a practical framework for setting your own emergency fund target — no jargon required.

What Does a 2.6% Savings Rate Actually Mean?

The personal savings rate is calculated by the U.S. Bureau of Economic Analysis. It measures what’s left of your disposable (after-tax) income after you’ve paid for everything — housing, food, transportation, utilities, and all the rest. At 2.6%, that means for every $1,000 in take-home pay, the average American is saving just $26.

To put that in perspective: if your household brings home $5,000 a month after taxes, a 2.6% savings rate means you’re setting aside about $130. That’s less than a typical car insurance payment in many states.

A low savings rate like this isn’t just a statistic — it’s a signal. It tells us that most households have very little financial cushion being added month by month. And when something unexpected happens — a car breaks down, a medical bill arrives, or hours get cut at work — there’s not much of a buffer to absorb the hit.

Where Americans Actually Stand on Emergency Savings

The savings rate paints the macro picture, but survey data from Empower fills in the human details — and they’re sobering.

According to Empower research, 1 in 3 Americans — specifically 32% — have no emergency savings fund at all. Not a single dollar set aside for a rainy day.

And 29% of Americans say they can’t afford an unexpected expense over $400. Think about that for a moment. A single trip to urgent care, a blown tire, or a broken appliance could be enough to derail their finances entirely.

The median emergency savings balance across all Americans is just $500. That’s the midpoint — half of Americans have more, half have less. For most households, $500 would cover maybe a week or two of basic living expenses, not the three to six months that financial experts typically recommend.

The generational breakdown is just as striking. Boomers have saved a median of $2,000 for emergencies — four times the overall median. Gen X sits at $500, matching the national median. Millennials come in lowest of all generations, with a median of just $300. Gen Z’s median is $400.

These numbers reflect a generation that entered the workforce during or after the 2008 financial crisis and has since navigated a pandemic, rapid inflation, and a volatile job market — all of which make saving consistently very difficult.

The Emotional Weight of an Empty Safety Net

This isn’t just about dollars and cents. The same Empower research found that 50% of Americans admit they’re stressed about their current level of emergency savings. Over half — 52% — wish they had started saving sooner.

That stress makes sense. When you don’t have a financial cushion, every unexpected bill becomes a crisis. You’re forced to choose between paying rent and fixing the car, or between buying groceries and covering a medical co-pay. It’s a mentally exhausting way to live.

Perhaps most telling: 42% of Americans say their current savings wouldn’t help them at all if they lost their job today. And 46% say their emergency savings account has less money in it than it did a year ago.

What’s Getting in the Way?

According to the Empower survey, the top barrier to building emergency savings is inflation and rising prices — cited by 39% of respondents. A full 63% say the rising cost of living has made it harder to build or maintain their emergency fund, and 58% say saving for emergencies feels “almost impossible” with how expensive everything is right now.

Those feelings line up with the savings rate data. When 2.6% of income is all that’s left after expenses, there simply isn’t much room to direct money toward a savings cushion — even when you know you should.

The most common unexpected financial events Americans faced in the past year, per Empower, include:

- Car repairs, cited by 26% of respondents

- Medical bills, cited by 24% of respondents

- Home repairs, cited by 19% of respondents

- Job loss or income reduction, cited by 14% of respondents

- Pet emergencies, cited by 11% of respondents

None of these are exotic scenarios. They’re everyday life. And they’re exactly what an emergency fund is designed to handle.

How Much Should You Actually Have Saved?

The widely cited rule of thumb is three to six months’ worth of living expenses — and it’s a solid starting point. Here’s how to apply it in practice.

Step 1: Calculate Your Monthly Essential Expenses

Add up only the non-negotiable costs: rent or mortgage, utilities, groceries, transportation, insurance, and minimum debt payments. Leave out dining out, subscriptions, and entertainment — in a true emergency, those get cut first.

Say your essential monthly expenses come to $3,000. Your emergency fund target range would be:

- Three-month target: $9,000

- Six-month target: $18,000

If those numbers feel overwhelming, that’s completely understandable. The important thing is to start — not to be perfect on day one.

Step 2: Calibrate to Your Situation

Not everyone needs the same cushion. A few factors that suggest you should aim for the higher end of the range:

- Variable or freelance income: If your paycheck fluctuates, you need more buffer for the slow months.

- Single income household: There’s no backup earner if you lose your job.

- Dependents: Kids, elderly parents, or pets raise the stakes of any financial disruption.

- Industry volatility: If layoffs are common in your field, a bigger cushion makes sense.

On the other hand, if you have a very stable government job, a working partner, and low fixed expenses, three months may be plenty.

Step 3: Set a Starter Goal First

The Empower data shows that 18% of Americans have savings that would cover less than one month of expenses. If you’re in that group, don’t fixate on the six-month target yet. Focus on hitting $1,000 first. Then $2,000. Then one month of expenses. Small wins build momentum.

Where Should You Keep Your Emergency Fund?

Your emergency fund has one job: be there when you need it. That means it needs to be:

- Liquid — you can access it quickly, ideally within a day or two

- Safe — not exposed to market swings

- Separate — not mixed in with your everyday checking account (out of sight, out of mind actually helps here)

High-yield savings accounts (HYSAs) are the most popular home for emergency funds, and for good reason. They keep your money accessible while earning more than a traditional savings account. Money market accounts are another option with similar accessibility.

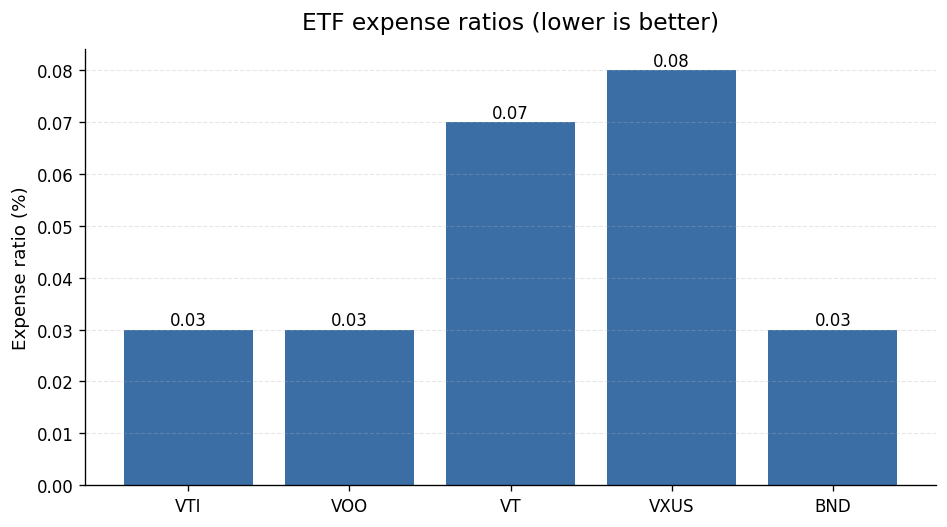

One thing worth being clear about: your emergency fund should NOT be invested in stocks or stock ETFs. Even low-cost, diversified funds like VTI (0.03% expense ratio) or VOO (0.03% expense ratio) are subject to significant market volatility. The whole point of an emergency fund is that it’s available and stable when you need it most — which is often during the same economic downturns that cause markets to fall. The same logic applies to international funds like VT (0.07% expense ratio) or VXUS (0.08% expense ratio), and even bond funds like BND (0.03% expense ratio) can lose value in rising-rate environments. Keep your emergency fund in cash or cash equivalents.

The Bright Spots: Awareness Is High

Despite the tough numbers, the Empower research shows that Americans aren’t checked out on this issue. A full 75% of Americans agree that emergency savings are essential for financial security, and 64% say building their emergency savings is a top financial priority right now.

Even better: 35% of Americans say the economic environment has actually caused them to increase their emergency fund contributions. And 31% say they’ve added to their emergency savings in the past month.

Awareness is the first step. Action is the second. If you’re reading this, you’ve already got the first part covered.

A Simple Action Plan to Build Your Emergency Fund

Here’s a straightforward path forward, regardless of where you’re starting from:

1. Open a dedicated savings account. Don’t keep your emergency fund in your checking account. A separate account — ideally a high-yield savings account — makes it easier to track and harder to accidentally spend.

2. Set a first milestone. If you have nothing saved, your first goal is $500. Then $1,000. Then one month of essential expenses. Celebrate each milestone — they matter.

3. Automate what you can. Even a small automatic transfer on payday — $25, $50, $100 — adds up over time. The Empower data shows that 17% of Americans contribute to their fund monthly as part of their budget. Automation takes the decision off your plate entirely.

4. Treat windfalls as accelerators. Tax refunds, bonuses, side hustle income — funnel a portion directly into your emergency fund before it gets absorbed into everyday spending.

5. Review and adjust annually. Your expenses change. Your income changes. Revisit your emergency fund target once a year to make sure it still reflects your actual life.

The Bottom Line

A personal savings rate of 2.6% is a warning sign — not a verdict. It tells us that most Americans are operating with very thin margins, and that the gap between where people are and where they need to be on emergency savings is real. But it also means there’s plenty of room to improve, and that small, consistent actions genuinely add up.

You don’t need three to six months of expenses saved by tomorrow. You just need to start — and keep going.

This article was researched using official U.S. data sources cited inline and reviewed for accuracy before publishing. It is general information, not personalized financial advice. For decisions specific to your situation, consult a licensed professional.

Data refreshed: 2026-05-29. Editorial accuracy verified for cited sources only.

Related reads

- Is Your Savings Account Actually Beating Inflation in 2026?

- High-Yield Savings Account Interest Taxes 2026: What You Owe the IRS

- Online Checking Accounts With No Fees and High APY: What to Look for in 2026

Armin Cole has been personally investing in index funds and ETFs

for over three years. He started Nestvestify to document what he’s

learning and make data-backed personal finance accessible to everyday

readers — without the jargon. All articles are grounded in official

U.S. data sources including the Federal Reserve (FRED), SEC filings,

and the Bureau of Labor Statistics.