Why the 10-Year Treasury Rate Matters to Index Fund Investors

If you own an index fund — whether it tracks the S&P 500, the total U.S. stock market, or a broad bond index — the 10-year Treasury yield is one of the most important numbers you can track. Yet most everyday investors scroll right past it. This guide breaks down what the rate actually is, how it connects to your portfolio, and what the current level means for your index fund strategy today.

What Is the 10-Year Treasury, Exactly?

The U.S. government borrows money by issuing Treasury securities. According to the U.S. Treasury and CD Wealth Management, there are three main types: Treasury bills (short-term, typically 4 to 52 weeks), Treasury notes (maturities from 2 to 10 years, with interest paid every six months), and Treasury bonds (long-term securities with maturities greater than 10 years, most commonly 30 years). The 10-year Treasury note sits in the middle of that range — it pays interest every six months and returns your principal after 10 years.

Because these securities are backed by the full faith and credit of the U.S. government, they rank among the safest investments available. The “yield” on the 10-year Treasury is simply the annualized return an investor would receive by buying one today and holding it to maturity.

As YCharts notes, many analysts use the 10-year yield as the “risk-free rate” when valuing stocks and other assets. That one fact explains why a shift in this single number can ripple across your entire portfolio.

Where Is the 10-Year Yield Right Now?

As of June 8, 2026, the 10-year Treasury Constant Maturity Rate stands at 4.56%. That’s a historically meaningful level — not extreme by the standards of past decades, but well above the near-zero rates that defined much of the 2010s.

For context, the weighted-average yield on outstanding U.S. Treasury bills, as reported by Treasury fiscal data, is 3.69% as of May 31, 2026. The gap between the 10-year yield at 4.56% and that short-term bill average reflects a more normal, upward-sloping yield curve — a sign that bond markets are pricing in longer-term growth and inflation expectations.

CD Wealth Management explains that the 10-year yield serves as a benchmark that influences borrowing costs across the board, from corporate bonds to mortgage rates and student loans. When this number moves, the effects spread throughout the economy and financial markets — including your index funds.

How the 10-Year Yield Connects to Your Stock Index Funds

You might be thinking: “I own VOO or VTI — why do I care about a government bond rate?” The answer comes down to how stocks are valued.

Analysts use the 10-year yield as a baseline risk-free rate. When that rate rises, the bar for what counts as an acceptable return from stocks rises with it. Investors may demand higher expected earnings from equities to justify the added risk of owning stocks instead of Treasuries. That pressure hits growth-oriented companies especially hard, since their value depends heavily on earnings projected years into the future.

CD Wealth Management notes that a common misconception is that when the Federal Reserve raises the federal funds rate, all interest rates move in lockstep — that’s generally not how it works. Short-term rates follow the federal funds rate, while longer-term rates like the 10-year yield are driven more by the market’s outlook on growth and inflation.

That distinction matters for index fund investors. Even if the Fed holds rates steady, the 10-year yield can drift higher if markets expect inflation to stick around or if the government issues large amounts of new debt. That kind of move can weigh on stock valuations with no Fed action required.

What This Means for VOO and VTI Specifically

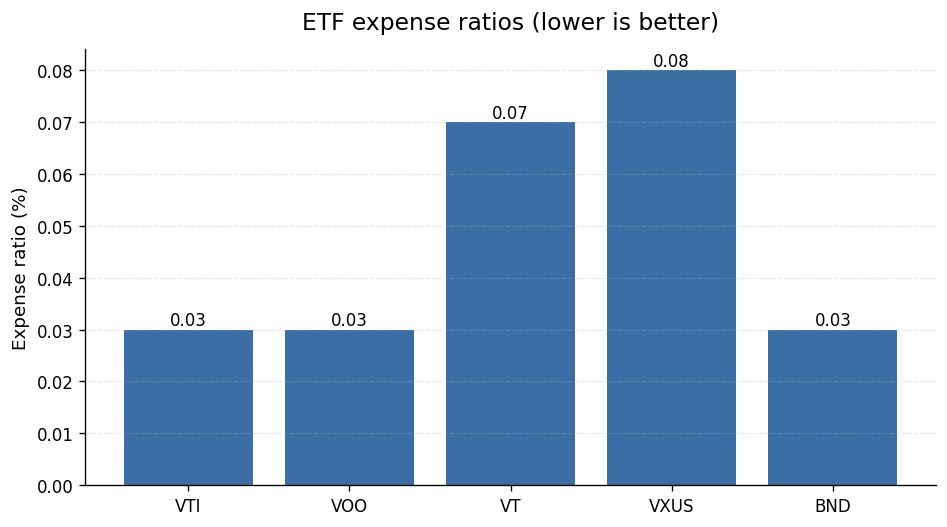

VOO (Vanguard S&P 500 ETF) most recently closed at $677.70 per share and carries an expense ratio of 0.03%. VTI (Vanguard Total Stock Market ETF) also carries an expense ratio of 0.03%. Those rock-bottom costs mean the funds themselves aren’t dragging on your returns — but broader market conditions, including where the 10-year yield sits, absolutely can be.

At a 4.56% risk-free rate, investors have a genuine alternative to stocks. A government-backed security paying 4.56% annually with essentially no credit risk is a far more meaningful competitor to equities than a 1% yield ever was. That doesn’t mean you should abandon your index funds — but it does mean stock valuations face more scrutiny than they did during the low-rate era.

How the 10-Year Yield Affects Your Bond Index Fund

If you hold a bond index fund like BND (Vanguard Total Bond Market ETF), the relationship with the 10-year yield is even more direct. BND carries an expense ratio of 0.03%.

Bond funds hold a large collection of existing bonds. When new bonds are issued at higher yields, the older bonds in the fund — which pay lower fixed coupons — become relatively less attractive, and their prices fall to compensate. That’s why rising yields tend to create short-term price pressure on bond funds.

There’s a silver lining that often gets overlooked, though: as older bonds mature and the fund reinvests in new, higher-yielding ones, the income the fund generates grows over time. Counterpoint Funds’ 2026 fixed income analysis describes this dynamic well — in today’s environment, fixed income returns are being driven more by “income carry” (the yield you collect) than by price appreciation. For long-term investors, that’s actually a healthy shift: you’re being paid more to wait.

The ‘Higher for Longer’ Rate Environment in 2026

Counterpoint Funds notes that the Federal Reserve has maintained a cautious stance in 2026, with inflation remaining the primary obstacle to rate cuts. Markets that entered the year expecting multiple cuts have since repriced toward fewer and later reductions. This “higher for longer” backdrop means bond fund investors should dial back expectations for big price gains — but can reasonably count on solid income from elevated starting yields.

For a diversified investor holding both stock and bond index funds, this environment isn’t a crisis. It just calls for recalibrated expectations. The income from your bond fund is more valuable than it was a few years ago.

International Index Funds: VT and VXUS

The 10-year yield also has implications if you hold international index funds. VT (Vanguard Total World Stock ETF) carries an expense ratio of 0.07%, while VXUS (Vanguard Total International Stock ETF) carries an expense ratio of 0.08%.

The 10-year yield shapes the relative attractiveness of U.S. assets versus foreign ones, which in turn affects currency values and cross-border capital flows. Those dynamics can add complexity to international fund returns when measured in U.S. dollars. That said, the long-term case for diversification through funds like VT or VXUS rests on factors that go well beyond any single year’s rate environment.

What Should You Actually Do?

Keeping tabs on the 10-year yield is worthwhile, but it shouldn’t send you scrambling to overhaul your portfolio every time the number moves. Here’s a plain-English framework for thinking through your situation:

1. Keep Your Expense Ratios in Check

The single most reliable lever you control is cost. VOO and VTI each charge 0.03% annually, and BND charges 0.03% as well. VT charges 0.07% and VXUS charges 0.08%. These are among the lowest costs available anywhere. Staying in low-cost index funds means the 10-year yield’s impact — good or bad — flows through to you without being eaten up by fees.

2. Rethink Your Bond Allocation Expectations (Not Your Bond Allocation)

With the 10-year Treasury at 4.56%, bonds are generating real income again. Counterpoint Funds points out that Treasury yields near 4% and above mean investors are “once again being paid to own duration and credit.” If you’ve been underweighting bonds because yields were too low to bother with, that calculation has changed. The income from a bond fund like BND now carries real weight.

3. Don’t Try to Time the Rate Cycle

Predicting where the 10-year yield will be in six months is genuinely hard — professional bond managers get it wrong all the time. Counterpoint Funds notes that fixed income markets in 2026 have already seen yields fall early in the year, then reverse higher as inflation concerns resurfaced. Trying to trade around those swings is a reliable way to lock in losses and miss recoveries.

4. Keep Your Time Horizon in Mind

If you’re investing toward a goal that’s 10, 20, or 30 years out, today’s 10-year yield is one data point in a very long story. The 10-year Treasury yield at 4.56% is worth noting, but your index fund’s long-term outcome will depend far more on your savings rate, your asset allocation, and your ability to stay invested through rough patches than on any single yield reading.

5. Use the Yield as a Sanity Check on Cash

One practical use of the 10-year rate: if you’re sitting on a lot of cash “waiting for the right moment” to invest, ask yourself whether that money is working as hard as it could. With the weighted-average Treasury bill yield at 3.69%, short-term government securities are paying real money. That doesn’t mean you should park everything in T-bills, but it’s a useful benchmark for evaluating whether your savings account is keeping pace.

The Bottom Line

The 10-year Treasury yield at 4.56% sets a meaningful backdrop for every index fund investor in 2026. It raises the bar for stock valuations, boosts the income potential of bond funds, and reflects a “higher for longer” rate environment that rewards patience and income collection over chasing price gains.

The good news: if you’re already holding low-cost, diversified index funds like VOO, VTI, BND, VT, or VXUS, you’re well-positioned to handle this environment. The funds’ minimal expense ratios — 0.03% for VOO and VTI, 0.03% for BND, 0.07% for VT, and 0.08% for VXUS — mean you keep nearly every dollar the market delivers. Stay diversified, keep costs low, and let the income from today’s elevated yields do its job over time.

This article was researched using official U.S. data sources cited inline and reviewed for accuracy before publishing. It is general information, not personalized financial advice. For decisions specific to your situation, consult a licensed professional.

Data refreshed: 2026-06-11. Editorial accuracy verified for cited sources only.

Related reads

- Should You Add International Stocks to Your Index Fund Portfolio When the US Dollar Is Strong in 2026?

- Strong US Economy in 2026: Should You Still Add VXUS or VT to Your Portfolio?

- Fidelity ZERO Funds vs Vanguard VTI: Is a 0% Expense Ratio Actually Better for Index Investors?

Armin Cole has been personally investing in index funds and ETFs

for over three years. He started Nestvestify to document what he’s

learning and make data-backed personal finance accessible to everyday

readers — without the jargon. All articles are grounded in official

U.S. data sources including the Federal Reserve (FRED), SEC filings,

and the Bureau of Labor Statistics.