Why Inflation Changes the ETF Conversation

Most of the time, choosing between VTI, VOO, and VT inside a Roth IRA comes down to personal preference — total market vs. large caps vs. global exposure. But when inflation is running hot, the choice gets more interesting. Inflation reshapes which kinds of stocks tend to hold up, whether international diversification helps or hurts, and how much your real returns actually keep pace with rising prices.

The latest reading shows U.S. annual inflation at 2.94% (source), and the Consumer Price Index sitting at 333.979 (source). That’s not the runaway inflation of a few years ago, but it’s enough to put a real dent in purchasing power over a long retirement horizon. Inside a Roth IRA, every basis point of real return matters even more — because your gains compound tax-free.

Let’s break down each fund, then look at how inflation specifically affects the case for each one.

The Three Funds at a Glance

VTI — Vanguard Total Stock Market ETF

VTI tracks the CRSP US Total Market Index, which covers nearly 100% of the investable U.S. stock market across all capitalization segments — large, mid, small, and micro caps (source). When you own VTI, you own a slice of thousands of U.S. companies, from the biggest names in tech down to small regional businesses.

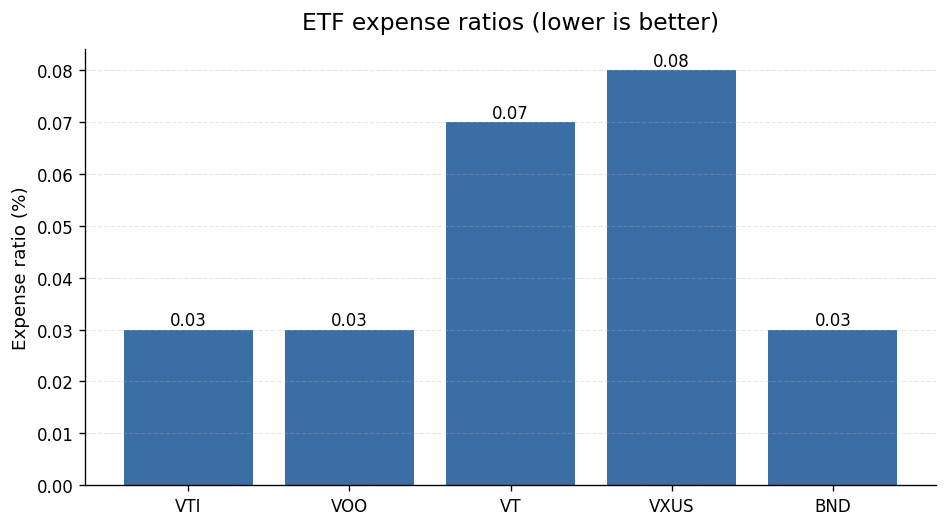

As of the most recent close, VTI was priced at $369.99 per share (source). Its expense ratio is just 0.03% (source) — meaning you pay $0.30 per year for every $1,000 invested. That’s about as cheap as investing gets.

The broad diversification of VTI is its biggest strength. Because it holds small and mid-cap stocks in addition to large caps, it gives you exposure to corners of the economy that VOO misses entirely.

VOO — Vanguard S&P 500 ETF

VOO tracks the S&P 500 Index (source), focusing on large, established U.S. companies. The S&P 500 is a market-cap-weighted index of 500 of the largest publicly traded U.S. firms, and VOO’s top 10 holdings represent about 30.78% of its total assets (source).

VOO’s latest close was $688.11 per share (source), and it carries the same 0.03% expense ratio as VTI (source). The S&P 500 recently closed at 7,500.58 (source), reflecting the index VOO is designed to mirror.

Because VOO concentrates on large-cap companies, it tends to be slightly more stable during market turbulence. Large companies often have more pricing power — meaning they can pass rising costs on to customers, which helps them hold up better when inflation picks up.

VT — Vanguard Total World Stock ETF

VT is the global version of VTI. Where VTI sticks to U.S. stocks, VT adds international exposure to the mix. Its expense ratio is 0.07% (source) — still very low by any standard, but more than double what VTI and VOO charge.

That extra cost reflects the added complexity of managing a global portfolio, and it’s worth understanding before you commit.

How Inflation Affects Each Fund Differently

Large Caps vs. Small Caps in an Inflationary Environment

VOO’s exclusive focus on large-cap stocks can work in its favor when prices are rising. Large companies — particularly those in sectors like energy, consumer staples, and financials — often have the scale and market position to raise prices without losing customers. That pricing power can translate into earnings that keep pace with inflation.

VTI holds those same large-cap stocks (the two funds overlap significantly at the top), but it also holds thousands of smaller companies. Small and mid-cap firms can struggle more during inflationary periods because they often face rising input costs without the same ability to pass them along. That said, some small-cap sectors — like energy producers and commodity-linked businesses — can actually outperform during inflation.

According to Forbes, VTI’s top 10 holdings represent 26.5% of its total assets, compared to 30.78% for VOO (source). VTI is more diversified, which smooths out volatility from any one sector — but it also means more exposure to parts of the market that may lag when inflation is elevated.

The International Wild Card: VT

VT’s global diversification is appealing in theory. Spreading your bets across the world means no single country’s economic cycle dominates your returns. In practice, though, the inflation story for VT is more complicated.

First, there’s the currency dimension. When U.S. inflation is high relative to other countries, the relative value of currencies can shift — and those shifts affect the dollar-denominated returns you see in your account. International returns can be boosted or dragged down by currency movements that have nothing to do with the underlying businesses.

Second, VT’s expense ratio of 0.07% (source) is higher than VTI’s and VOO’s 0.03% (source). In a low-return environment driven by inflation-squeezed earnings, every extra basis point you pay in fees drags on your real returns.

Third — and this matters specifically for Roth IRA holders — international funds like VT pay dividends that may have foreign taxes withheld at the source. In a taxable brokerage account, you may be able to claim a foreign tax credit to offset some of that withholding. Inside a Roth IRA, that option isn’t available in the same way, so any withheld taxes on foreign dividends become a permanent cost.

The Roth IRA Advantage — and Why It Amplifies This Decision

A Roth IRA is one of the most powerful accounts available to everyday investors. The IRS sets the annual contribution limit at $7,000 for tax year 2025 (source), with a $1,000 catch-up contribution for those age 50 and older (source), bringing the max to $8,000 for that group.

Because a Roth IRA grows tax-free and qualified withdrawals aren’t taxed, the compounding effect over decades is significant. But that also means any drag on returns — whether from fees, foreign tax leakage, or a fund that lags inflation — compounds in the wrong direction too.

Here’s a simple way to think about it: if inflation is running at 2.94% (source) and your fund’s real return is further reduced by a higher expense ratio, you’re losing ground on two fronts. The Roth IRA’s tax-free growth is most valuable when you maximize the real return inside it.

Comparing the Costs Side by Side

Expense ratios might seem like a minor detail, but over a 20- or 30-year Roth IRA horizon, they add up. Here’s a quick comparison:

| Fund | Expense Ratio | Source |

|---|---|---|

| VTI | 0.03% | Vanguard |

| VOO | 0.03% | Vanguard |

| VT | 0.07% | Vanguard |

VTI and VOO are tied on cost. VT costs more than twice as much — which is still cheap in absolute terms, but the difference matters when you’re trying to outrun inflation.

For context, the average yield on outstanding U.S. Series I Savings Bonds — a popular inflation-protection tool — is 4.383% (source). I Bonds are a separate asset class entirely, but that yield gives you a useful benchmark for what inflation protection looks like in practice. Equity ETFs like VTI, VOO, and VT aren’t designed to track inflation directly — they’re designed to grow wealth over time, which historically has outpaced inflation over long periods.

So Which ETF Actually ‘Wins’ When Inflation Is High?

There’s no single winner for every investor. But there are some clear patterns worth knowing.

If you want simplicity and low cost: VTI or VOO

Both VTI and VOO carry a 0.03% expense ratio (source) (source), and both give you broad U.S. equity exposure. During inflationary periods, U.S. large-cap stocks have historically shown more pricing power than small caps or many international markets. VOO leans more heavily into that large-cap advantage, while VTI adds breadth.

For most Roth IRA investors who want to set it and forget it, either VTI or VOO is a strong choice. The difference in long-term returns between the two has historically been very small, according to Forbes (source).

If you want global diversification: VT, but understand the trade-offs

VT makes sense if you believe international markets will outperform U.S. markets over your investment horizon, or if you simply want to reduce your concentration in any one country. But in a high-inflation U.S. environment, the foreign tax leakage inside a Roth IRA and the higher 0.07% expense ratio (source) are real headwinds.

One alternative some investors use: hold VTI (or VOO) for U.S. exposure and add VXUS — the Vanguard Total International Stock ETF, which carries a 0.08% expense ratio (source) — separately. This gives you more control over your domestic vs. international allocation rather than letting VT decide for you.

The inflation-protection angle in a Roth IRA

If protecting purchasing power is your primary concern, equities are generally a better long-term hedge against inflation than cash or bonds. The U.S. real interest rate was -1.09% as recently as the data available (source), which shows how easily inflation can erode returns on fixed-income or cash-equivalent holdings.

Inside a Roth IRA, tax-free compounding amplifies whatever real return your fund generates. Choosing a fund with low fees and broad exposure to companies that can grow earnings in an inflationary environment is the most direct path to protecting your purchasing power over time.

A Practical Framework for Deciding

Here’s a simple decision guide based on your priorities:

Choose VOO if: You want to concentrate on large, established U.S. companies with strong pricing power and you’re comfortable with less small-cap exposure.

Choose VTI if: You want the broadest possible U.S. market exposure, including small and mid caps, at the same ultra-low cost as VOO.

Choose VT if: You genuinely want global diversification in a single fund and you’re comfortable with the slightly higher expense ratio and the foreign tax dynamics inside a Roth IRA.

Consider VTI + VXUS if: You want global exposure but prefer to control your U.S. vs. international split manually. VXUS carries a 0.08% expense ratio (source).

The Roth IRA annual contribution limit is $7,000 for tax year 2025 (source), so every dollar you contribute counts. Keeping costs low and staying invested in broadly diversified equities is the foundation of a solid inflation-fighting strategy inside this account.

The Bottom Line

When inflation is elevated, the edge goes to funds with low costs, strong exposure to companies with pricing power, and minimal fee drag. VTI and VOO both check those boxes with their 0.03% expense ratios (source) (source). VT is a solid choice for global diversification, but its 0.07% expense ratio (source) and the foreign tax dynamics inside a Roth IRA make it a harder sell when inflation is running hot.

The most important thing you can do is stay invested, keep costs low, and let the Roth IRA’s tax-free compounding work in your favor over the long haul.

This article was researched using official U.S. data sources cited inline and reviewed for accuracy before publishing. It is general information, not personalized financial advice. For decisions specific to your situation, consult a licensed professional.

Data refreshed: 2026-06-22. Editorial accuracy verified for cited sources only.

Related reads

- What the 10-Year Treasury Rate Means for Your Index Fund Returns in 2026

- CD vs. Treasury Bills: Is Locking Into a CD Still Worth It When T-Bill Rates Are This High?

- Should You Add International Stocks to Your Index Fund Portfolio When the US Dollar Is Strong in 2026?

Armin Cole has been personally investing in index funds and ETFs

for over three years. He started Nestvestify to document what he’s

learning and make data-backed personal finance accessible to everyday

readers — without the jargon. All articles are grounded in official

U.S. data sources including the Federal Reserve (FRED), SEC filings,

and the Bureau of Labor Statistics.