Why Inflation Is the Invisible Tax on Your Portfolio

You check your index fund and see it’s up. Great news, right? Maybe. What really matters isn’t the number on your screen — it’s how much purchasing power that number represents after inflation takes its cut. Inflation is sometimes called an invisible tax because it doesn’t show up as a line item on your brokerage statement, yet it quietly erodes what your money can actually buy.

This guide walks you through how inflation measured in 2025–2026 affects the real-world value of your index fund returns, which funds are best positioned to hold their ground, and what practical steps you can take to protect your long-term wealth.

What the CPI Actually Measures

The Consumer Price Index for All Urban Consumers (CPI-U) is the government’s main inflation yardstick. According to the U.S. Bureau of Labor Statistics via FRED, the CPI-U tracks a basket of goods and services — including food, clothing, shelter, fuels, transportation fares, and service fees — paid by urban consumers. It covers roughly 88 percent of the total U.S. population, accounting for wage earners, retirees, the self-employed, and many others.

The index is expressed relative to a baseline period. As of April 2026, the seasonally adjusted CPI-U stood at 332.407 (Index 1982–1984 = 100). The unadjusted CPI-U for the same period came in at 333.02 (Index 1982–84 = 100). In plain terms: prices today are more than three times what they were during the early 1980s baseline period.

Why does this matter for index fund investors? Because every percentage point of inflation is a percentage point of return you need to earn back just to stay even.

Nominal Returns vs. Real Returns: The Core Concept

Your nominal return is the raw number your brokerage shows you. Your real return is what’s left after inflation. If your index fund gains 8 percent in a year and inflation runs at 3 percent, your real gain is roughly 5 percent — that’s the actual increase in your purchasing power.

The World Bank’s most recent annual figure for U.S. consumer price inflation (for the full year ending December 2024) was 2.95 percent. Even a “moderate” inflation rate of roughly 3 percent means an index fund needs to return more than 3 percent just to break even in real terms.

The World Bank also tracks the U.S. real interest rate — the nominal interest rate minus inflation. As of the end of 2021, the U.S. real interest rate was –1.09 percent, meaning that after accounting for inflation, many traditional savings vehicles were actually losing ground. That specific data point is a few years old, but it illustrates a recurring pattern: when inflation spikes, real rates can turn negative, and savers who park money in low-yield accounts pay a steep hidden price.

How Inflation Affects Different Types of Index Funds

Not all index funds respond to inflation the same way. Here’s a plain-English breakdown.

Stock Index Funds: Your Best Long-Run Inflation Hedge

Broad stock market index funds — think funds that track the S&P 500 or the total U.S. stock market — have historically been among the strongest long-run defenses against inflation. The companies inside those funds can often raise prices when their own costs go up, passing inflation along to customers and protecting their earnings.

Two of the most popular options are VOO and VTI:

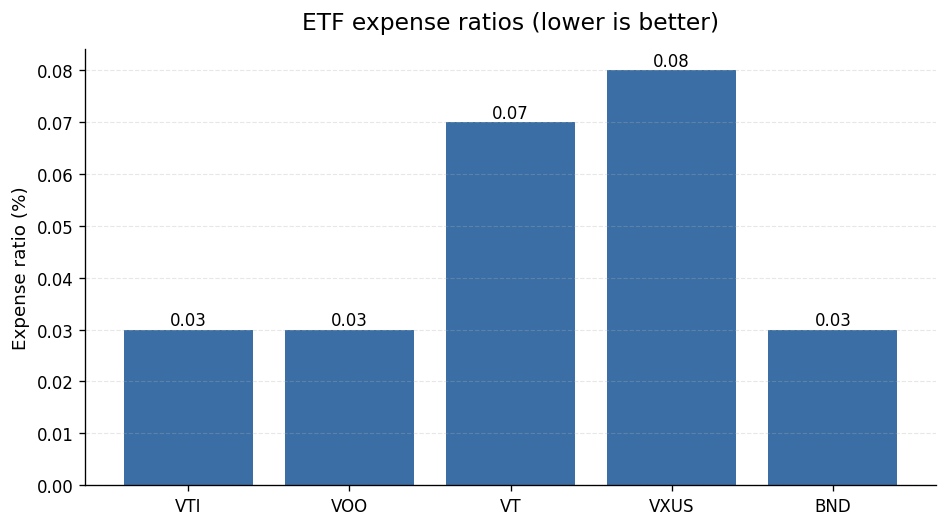

- VOO (Vanguard S&P 500 ETF) carries an expense ratio of just 0.03% and most recently closed at $678.00 per share (as of June 5, 2026).

- VTI (Vanguard Total Stock Market ETF) also carries an expense ratio of 0.03%, giving you exposure to large-, mid-, and small-cap U.S. stocks in a single fund.

Those razor-thin expense ratios matter more during inflationary periods. Every basis point you don’t pay in fees is a basis point that stays in your account compounding against inflation.

International Stock Index Funds: Spreading the Risk

Adding international exposure can help because inflation doesn’t always move in lockstep across countries. If U.S. inflation is elevated while another region’s is tamer, international holdings may hold their real value better.

- VT (Vanguard Total World Stock ETF) gives you both U.S. and international stocks in one fund, with an expense ratio of 0.07%.

- VXUS (Vanguard Total International Stock ETF) covers non-U.S. stocks specifically, with an expense ratio of 0.08%.

Both are still low-cost options, though slightly higher than the domestic-only funds above.

Bond Index Funds: More Vulnerable to Inflation

Bond index funds face a tougher environment when inflation is elevated. Fixed coupon payments lose purchasing power when prices are rising, and rising interest rates — which often accompany inflation — push existing bond prices down. That’s a fundamental mechanical relationship in fixed-income markets.

- BND (Vanguard Total Bond Market ETF) has an expense ratio of 0.03%, which helps cushion the blow, but it doesn’t eliminate inflation risk in the underlying bonds.

Bonds still play a useful role in a diversified portfolio — they provide stability and income even when their real returns are compressed during inflationary stretches.

A Practical Look at Real Returns

Here’s a concrete example. Suppose your broad stock index fund delivers a hypothetical nominal return of 9 percent in a given year. If inflation is running near the World Bank’s most recent annual figure of 2.95 percent for the U.S., your approximate real return is about 6 percent. That’s still strong — but it’s meaningfully less than the headline number.

Now consider a bond fund returning 4 percent in the same environment. After roughly 3 percent inflation, your real gain is closer to 1 percent. And if inflation were to push higher, that bond fund could be treading water or even losing real ground.

This math is why long-term investors generally keep a meaningful allocation to stock index funds — they offer the best realistic shot at returns that outpace inflation over decades, even if they’re more volatile year to year.

The Compounding Effect: Why Inflation Damage Grows Over Time

Inflation’s impact on your portfolio isn’t just a one-year problem — it compounds. When inflation averages even 3 percent a year over 20 years, the purchasing power of a dollar falls to roughly 55 cents. An index fund that earns 6 percent nominally but faces 3 percent inflation annually is only building about half the real wealth it appears to be building on paper.

This compounding erosion is why the difference between a 2 percent and a 4 percent inflation rate — which sounds small — can mean tens of thousands of dollars in real purchasing power over a 30-year retirement horizon.

The takeaway: don’t just watch your account balance grow. Watch your real return — the nominal gain minus inflation.

What About Inflation-Linked Alternatives?

Some investors turn to inflation-linked instruments as a complement to index funds. One example is U.S. Series I Savings Bonds. As of May 31, 2026, the average yield on outstanding U.S. Series I Savings Bonds was 4.383%, according to Treasury fiscal data. That yield reflects both a fixed component and an inflation adjustment, which is why I Bonds can be appealing when inflation is elevated.

That said, I Bonds come with purchase limits and liquidity restrictions that make them a supplement to — not a replacement for — a diversified index fund portfolio.

Keeping Costs Low Is an Inflation Strategy

Here’s something many investors overlook: minimizing fund expenses is itself an inflation-fighting move. Every dollar you save on fees is a dollar that stays invested and compounds. When inflation is elevated, that compounding matters even more because you need every basis point of return working for you.

Look at the expense ratios of the funds mentioned above:

| Fund | Expense Ratio |

|---|---|

| VOO (S&P 500) | 0.03% |

| VTI (Total Stock Market) | 0.03% |

| BND (Total Bond Market) | 0.03% |

| VT (Total World Stock) | 0.07% |

| VXUS (Total International) | 0.08% |

These are some of the lowest-cost funds available to everyday investors. At 0.03 percent, you’re paying just $3 per year on every $10,000 invested. A fund charging 1 percent would cost $100 per year on the same balance — and that $97 difference compounds against you every single year, working alongside inflation to shrink your real wealth.

Practical Steps to Protect Your Index Fund Returns from Inflation

1. Stay Invested in Broad Stock Index Funds

The single most effective long-run inflation hedge for most people is staying invested in low-cost, diversified stock index funds. Sitting in cash during inflationary periods is one of the costliest mistakes an investor can make, because cash loses purchasing power in real time.

2. Keep Expense Ratios as Low as Possible

The difference between a 0.03% and a 1% expense ratio is enormous over decades. Stick to low-cost index funds and let compounding work for you, not against you.

3. Rebalance Thoughtfully

Inflation affects different asset classes differently. Stocks tend to hold up better; bonds tend to struggle more. Periodic rebalancing — bringing your portfolio back to your target allocation — ensures you’re not accidentally overexposed to the asset class most hurt by inflation.

4. Consider Your Bond Allocation Carefully

A heavy bond allocation can drag down your real returns if inflation stays elevated. That doesn’t mean eliminating bonds — they still provide stability — but it’s worth reviewing whether your bond allocation matches your inflation outlook and time horizon.

5. Use Tax-Advantaged Accounts

Inflation erodes real returns. Taxes erode nominal returns. Using tax-advantaged accounts like IRAs and 401(k)s means more of your nominal return survives to compound, giving you a better shot at meaningful real gains.

The Bottom Line

Inflation measured by the CPI-U — which stood at 332.407 (seasonally adjusted) and 333.02 (unadjusted) as of April 2026 — is a real and ongoing force working against your purchasing power. The World Bank’s most recent annual U.S. inflation figure of 2.95 percent (for the year ending December 2024) is a reminder that even “moderate” inflation meaningfully reduces real returns over time.

The good news: low-cost, diversified stock index funds remain one of the most accessible and effective tools everyday investors have to stay ahead of inflation over the long run. Keep costs low, stay diversified, and focus on real returns — not just the numbers on your screen.

This article was researched using official U.S. data sources cited inline and reviewed for accuracy before publishing. It is general information, not personalized financial advice. For decisions specific to your situation, consult a licensed professional.

Data refreshed: 2026-06-08. Editorial accuracy verified for cited sources only.

Related reads

- VTI vs SCHB vs SPLG: Which Total Market ETF Costs Less for a Roth IRA in 2026?

- Does FDIC Insurance Cover Online Checking and Money Market Accounts? A Plain-English FAQ

- CD Ladder Strategy for 2026: How to Use Treasury Rates as Your Benchmark

Armin Cole has been personally investing in index funds and ETFs

for over three years. He started Nestvestify to document what he’s

learning and make data-backed personal finance accessible to everyday

readers — without the jargon. All articles are grounded in official

U.S. data sources including the Federal Reserve (FRED), SEC filings,

and the Bureau of Labor Statistics.