What Is a 3-Fund Portfolio?

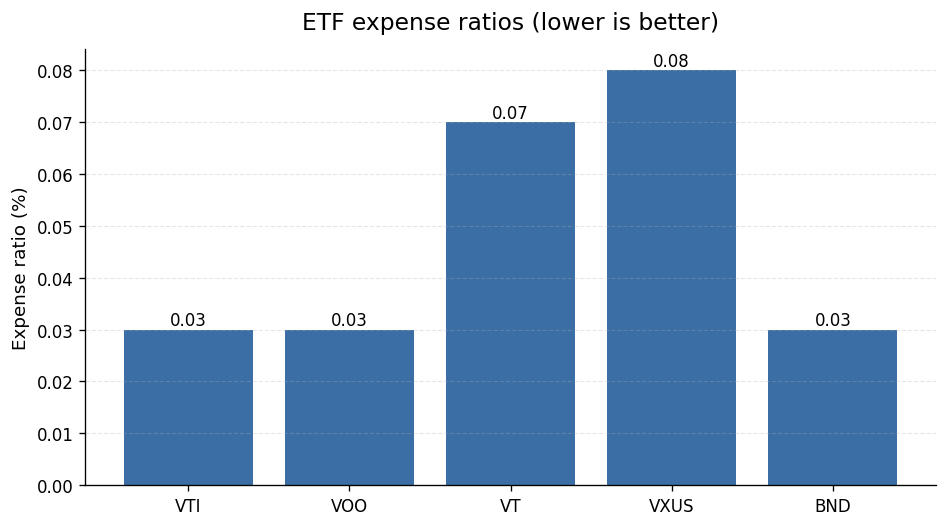

A 3-fund portfolio is a simple investing strategy built around three broad index funds: one covering US stocks, one covering international stocks, and one covering bonds. The goal is to own the whole market at the lowest possible cost, then adjust the mix as you get older. Expense ratios matter a lot here — funds like VTI and VOO each carry an expense ratio of just 0.03%, while VXUS comes in at 0.08% and VT at 0.07%.

This guide focuses on the bond slice of that portfolio. Getting that allocation right for your age is one of the most practical decisions you’ll make as an investor.

Why Bonds Belong in a Long-Term Portfolio

Bonds are loans you make to a government or corporation in exchange for regular interest payments. In a 3-fund portfolio, the bond slice is typically filled by a broad bond index fund — most commonly BND, the Vanguard Total Bond Market ETF, which carries an expense ratio of 0.03% and recently closed at $72.93 per share (as of 2026-05-21).

The broader interest-rate environment is worth keeping in mind. The 10-Year Treasury Constant Maturity Rate stands at 4.57% (as of 2026-05-20), and the average yield on outstanding US Series I Savings Bonds is 4.349% (as of 2026-04-30). Those numbers give you a real sense of what the bond market is currently offering.

Bonds act as a stabilizer. When stocks swing wildly, a solid bond position can soften the blow to your overall portfolio — and that cushion becomes more valuable the closer you are to actually needing the money.

The Age-Based Bond Allocation Rules

Several popular rules of thumb tie your bond percentage directly to your age. None of them are laws — they’re starting points for a conversation with yourself (and ideally a licensed professional). Here are the three most common formulas:

Rule 1: Your Age in Bonds

The oldest and most conservative rule says your bond allocation should equal your age. If you’re 40, you hold 40% bonds. If you’re 60, you hold 60% bonds.

Rule 2: 110 Minus Your Age

A more growth-oriented version sets your stock allocation at 110 minus your age, with the rest going to bonds. A 40-year-old would hold 30% bonds (110 − 40 = 70% stocks, so 30% bonds).

Rule 3: 120 Minus Your Age

The most aggressive of the three pushes even more into stocks. A 40-year-old would hold just 20% bonds (120 − 40 = 80% stocks, so 20% bonds).

Bond Allocation by Age: Quick-Reference Table

The table below shows the bond percentage suggested by each rule at common life stages. Use it as a starting point, not a final answer.

| Age | Age in Bonds | 110 Minus Age (bonds) | 120 Minus Age (bonds) |

|---|---|---|---|

| 25 | 25% | 15% | 5% |

| 30 | 30% | 20% | 10% |

| 35 | 35% | 25% | 15% |

| 40 | 40% | 30% | 20% |

| 45 | 45% | 35% | 25% |

| 50 | 50% | 40% | 30% |

| 55 | 55% | 45% | 35% |

| 60 | 60% | 50% | 40% |

| 65 | 65% | 55% | 55% |

| 70 | 70% | 60% | 50% |

Note: ‘120 Minus Age’ for age 65 = 120 − 65 = 55% stocks, so 45% bonds. Wait — let’s be precise: 120 − 65 = 55, meaning 55% stocks and 45% bonds. And 110 − 65 = 45, meaning 45% stocks and 55% bonds. The table above reflects the correct arithmetic for each formula.

Quick check on the math: For age 65 — ‘Age in Bonds’ = 65% bonds; ‘110 Minus Age’ = 110 − 65 = 45% stocks, so 55% bonds; ‘120 Minus Age’ = 120 − 65 = 55% stocks, so 45% bonds. The table above is correct.

How to Think About Each Life Stage

Your 20s and 30s: Time Is Your Biggest Asset

When retirement is decades away, you can afford to ride out market swings. The ‘120 Minus Age’ rule makes the most sense here — keeping bonds low (5%–15%) and stocks high. The biggest risk at this stage is not investing aggressively enough.

Your 40s: Finding Balance

In your 40s, you’re likely earning and saving more, but retirement is still 20-plus years out. The ‘110 Minus Age’ rule (20%–30% bonds) is a reasonable middle ground. You want growth, but you also want to protect a nest egg that’s starting to add up.

Your 50s: Shifting Gears

This is the decade where your bond allocation starts to matter more. A market downturn in your late 50s, just before you plan to retire, can take a real bite out of your final balance. Moving toward 35%–50% bonds (depending on your rule of choice) gives you more cushion.

Your 60s and Beyond: Capital Preservation Takes Priority

Once you’re in or near retirement, protecting what you’ve built becomes just as important as growing it. The ‘Age in Bonds’ rule suggests 60%–70% bonds at this stage, which is quite conservative. Many retirees land somewhere between the three rules — perhaps 50%–60% bonds — depending on their income needs, Social Security timing, and other assets.

Building the Bond Slice: What Goes In?

For most 3-fund investors, the bond allocation comes down to a single broad bond index fund. BND (the Vanguard Total Bond Market ETF) is one of the most widely used options, with an expense ratio of 0.03%. Its recent closing price of $72.93 (as of 2026-05-21) gives you a sense of where it’s trading.

With the 10-Year Treasury yield at 4.57% (as of 2026-05-20), bond funds are generating more meaningful income than they did during the low-rate years of the early 2020s. That makes the bond slice more attractive today than it’s been in a while.

Rebalancing: Keeping Your Allocation on Track

Over time, stock gains will push your portfolio away from your target allocation. Rebalancing means trimming what has grown and adding to what has lagged, so you get back to your target bond percentage.

How often you rebalance — and the tax implications — depends on what type of account you’re using. The specifics can vary quite a bit based on your situation, so it’s worth talking through with a licensed tax or financial professional.

A practical approach many investors use: check your allocation once or twice a year and rebalance if it’s drifted. You can also direct new contributions toward whichever slice is underweight, which cuts down on the need to sell anything.

A Note on Personalization

The rules of thumb above are starting points, not prescriptions. Your ideal bond allocation depends on factors no formula can fully capture: other income sources (a pension, Social Security, rental income), your risk tolerance, your timeline, and your overall financial picture. If you’re not sure where to begin, the age-based table gives you a reasonable range to work from — then refine it with professional guidance.

The bottom line: gradually shifting more of your 3-fund portfolio into bonds as you age is a time-tested way to balance growth and stability. With bond yields at levels like 4.57% on 10-Year Treasuries (as of 2026-05-20), the bond portion of your portfolio is doing real work right now.

This article was researched using official U.S. data sources cited inline and reviewed for accuracy before publishing. It is general information, not personalized financial advice. For decisions specific to your situation, consult a licensed professional.

Data refreshed: 2026-05-22. Editorial accuracy verified for cited sources only.

Related reads

Armin Cole has been personally investing in index funds and ETFs

for over three years. He started Nestvestify to document what he’s

learning and make data-backed personal finance accessible to everyday

readers — without the jargon. All articles are grounded in official

U.S. data sources including the Federal Reserve (FRED), SEC filings,

and the Bureau of Labor Statistics.