The Striking Gap Between These Two Accounts

If you’ve ever wondered why your 401(k) feels like the “big” retirement account and your Roth IRA feels like a side dish, the contribution limits tell the whole story. For tax year 2025, you can put up to $23,500 into a 401(k) (IRS) but only $7,000 into a Roth IRA (IRS). That’s more than a three-to-one difference.

Both accounts let your money grow tax-advantaged, but they work very differently — and the rules around contribution limits, eligibility, and retirement withdrawals don’t overlap as much as people assume. This side-by-side guide breaks it all down in plain English.

The 2025 Contribution Limits at a Glance

401(k) Limits for 2025

The employee elective deferral limit for a 401(k) — or a 403(b), which works the same way — is $23,500 for tax year 2025 (IRS). That’s the most you, as an employee, can contribute from your own paycheck.

If you’re age 50 or older by the end of the year, you can add a catch-up contribution of $7,500 on top of that (IRS), bringing your total potential employee contribution to $31,000.

One rule worth knowing: the $23,500 limit is per individual, not per employer. If you change jobs mid-year and contribute to two different 401(k) plans, your combined contributions across both plans still can’t exceed $23,500 (IRS). Go over that, and if the excess isn’t returned to you by April 15 of the following year, you could face double taxation — once in the year you deferred the money, and again when you take a distribution (IRS).

Roth IRA Limits for 2025

The annual contribution limit for a Roth IRA in 2025 is $7,000 (IRS). If you’re age 50 or older, you can tack on an extra $1,000 as a catch-up, for a total of $8,000 (IRS).

Those limits are much smaller than the 401(k), but the Roth IRA comes with some distinct advantages covered below.

Quick-Reference Table

| 401(k) / 403(b) | Roth IRA | |

|---|---|---|

| 2025 base limit | $23,500 | $7,000 |

| Catch-up (age 50+) | $7,500 | $1,000 |

| Total with catch-up | $31,000 | $8,000 |

| Income limits? | No | Yes |

| Tax on contributions | Pre-tax (traditional) or after-tax (Roth 401k) | After-tax only |

| RMDs required? | Yes | No (owner’s lifetime) |

How the Two Accounts Are Taxed Differently

This is where the real difference lives — not just in the numbers, but in when you pay taxes.

401(k): Pay Taxes Later

Traditional 401(k) contributions are made with before-tax dollars (IRS). The money comes out of your paycheck before income taxes are applied, which lowers your taxable income today. The trade-off: withdrawals in retirement are taxed as ordinary income.

Many employers also offer a Roth 401(k) option. Roth 401(k) contributions are made with after-tax dollars (IRS), so you don’t get the upfront tax break — but qualified withdrawals in retirement are tax-free, just like a Roth IRA.

Roth IRA: Pay Taxes Now, Withdraw Tax-Free Later

Roth IRA contributions are always made with after-tax dollars (IRS). You don’t get a deduction today, but your money grows tax-free. When you take a qualified distribution — meaning the account has been open for at least five years and you’re age 59½ or older, or the withdrawal is due to disability or death — neither your contributions nor your earnings are taxed (IRS).

The Roth IRA also has a qualified distribution option the 401(k) doesn’t match: you can use funds for a first-time home purchase (IRS).

The Income Limit Hurdle: Who Can Use a Roth IRA?

Here’s the big catch with the Roth IRA: not everyone can contribute directly, depending on how much they earn. The 401(k) has no income limits to participate (IRS), but the Roth IRA does.

For the 2024 tax year, the IRS phased out Roth IRA eligibility for single filers with a modified adjusted gross income (MAGI) between $146,000 and $161,000 — above $161,000, single filers could contribute nothing (IRS). For married filing jointly, the phase-out range ran from $230,000 to $240,000 — above $240,000, the contribution was zero (IRS).

These thresholds are adjusted periodically, so always check the current IRS guidance for the tax year you’re filing.

If your income is too high to contribute directly to a Roth IRA, the 401(k) has no such restriction (IRS), making it accessible to virtually any employed person regardless of earnings.

Required Minimum Distributions: A Key Retirement Difference

Once you hit a certain age, the IRS generally requires you to start pulling money out of your retirement accounts — these are called required minimum distributions (RMDs).

For a traditional 401(k) and a designated Roth 401(k), distributions must begin no later than age 72 (unless you’re still working and not a 5% owner of the business) (IRS). Yes, even the Roth 401(k) is subject to RMDs.

The Roth IRA is different: there is no requirement to start taking distributions while the owner is alive (IRS). Your money can keep compounding for as long as you live without being forced out. That makes the Roth IRA especially useful for people who don’t need the money right away in retirement and want to let it keep growing.

Can You Contribute to Both a 401(k) and a Roth IRA in the Same Year?

Yes — and for many people, doing both makes a lot of sense. The 401(k) and Roth IRA limits are completely separate from each other. Maxing out your 401(k) at $23,500 doesn’t reduce how much you can put into a Roth IRA (IRS).

So if you’re under 50 and your income falls within the Roth IRA limits, you could contribute $23,500 to your 401(k) and $7,000 to your Roth IRA in the same year — a combined $30,500 in retirement savings. If you’re 50 or older, those numbers rise to $31,000 (401(k)) plus $8,000 (Roth IRA).

The 401(k) limit applies across all your 401(k) and 403(b) plans combined in a given year (IRS), so if you have multiple plans, keep a close eye on your running total.

What Can You Invest In?

Once money is inside either account, it can be invested in a wide range of assets. Many people gravitate toward low-cost index funds and ETFs because they keep fees minimal, leaving more of your money to compound over time.

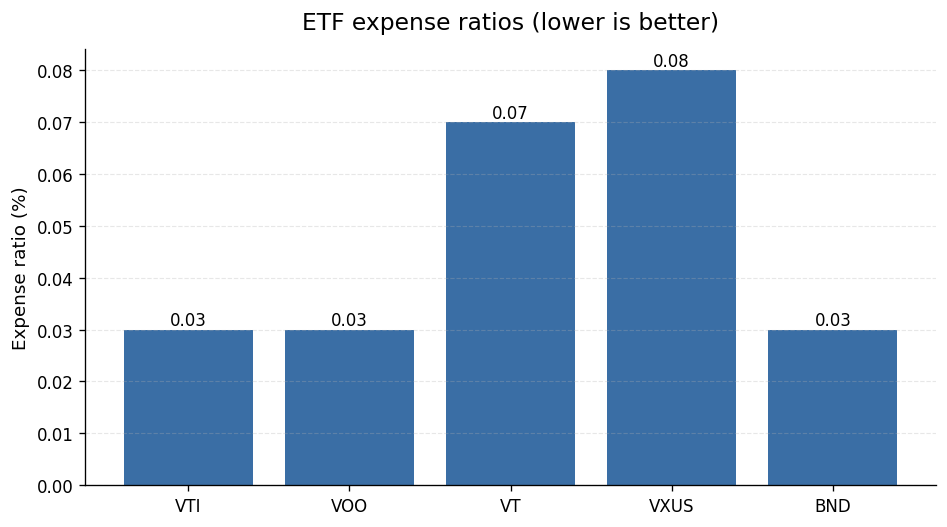

Popular Vanguard ETFs, for example, carry very low expense ratios:

- VTI (Vanguard Total Stock Market ETF): 0.03% expense ratio (Vanguard)

- VOO (Vanguard S&P 500 ETF): 0.03% expense ratio (Vanguard)

- BND (Vanguard Total Bond Market ETF): 0.03% expense ratio (Vanguard)

- VT (Vanguard Total World Stock ETF): 0.07% expense ratio (Vanguard)

- VXUS (Vanguard Total International Stock ETF): 0.08% expense ratio (Vanguard)

These funds are commonly used inside Roth IRAs opened at major brokerages. The investment options inside a 401(k) depend on the plan your employer has set up, so your menu may look different.

Practical Tips for Choosing Between the Two

Start With Any Employer Match

If your employer matches 401(k) contributions up to a certain percentage, contributing at least enough to capture the full match is a foundational move — that match is part of your total compensation.

Think About Your Tax Situation

If you expect to be in a higher tax bracket in retirement than you are now, the Roth IRA’s after-tax contributions and tax-free withdrawals can be a real advantage. If you’d rather cut your tax bill today, the traditional pre-tax 401(k) lowers your current taxable income.

Watch the Income Limits

If your income is near or above the Roth IRA phase-out thresholds, check the IRS guidance for the specific tax year (IRS) to find out whether you can contribute the full amount, a reduced amount, or nothing at all.

Factor In the RMD Rules When Planning for Retirement

If you want maximum flexibility in retirement — the ability to leave money in the account as long as you wish without forced withdrawals — the Roth IRA’s no-RMD-during-lifetime rule (IRS) gives it a clear edge for that goal.

The Bottom Line

The 401(k) wins on raw contribution room: $23,500 versus $7,000 for the Roth IRA in 2025. The Roth IRA wins on flexibility: no income taxes on qualified withdrawals, no required minimum distributions during your lifetime, and the option to use funds for a first-time home purchase as a qualified distribution.

For most people, the smartest move isn’t picking one over the other — it’s using both accounts together, each doing what it does best. The 401(k) gives you a large tax-advantaged bucket to fill; the Roth IRA gives you a tax-free pool of money to draw from in retirement on your own schedule.

Always verify the current year’s limits and income thresholds directly with the IRS, since these figures are adjusted over time.

This article was researched using official U.S. data sources cited inline and reviewed for accuracy before publishing. It is general information, not personalized financial advice. For decisions specific to your situation, consult a licensed professional.

Data refreshed: 2026-06-22. Editorial accuracy verified for cited sources only.

Related reads

- VTI vs VOO vs VT in a Roth IRA: Which ETF Wins When Inflation Is High?

- What the 10-Year Treasury Rate Means for Your Index Fund Returns in 2026

- Should You Add International Stocks to Your Index Fund Portfolio When the US Dollar Is Strong in 2026?

Armin Cole has been personally investing in index funds and ETFs

for over three years. He started Nestvestify to document what he’s

learning and make data-backed personal finance accessible to everyday

readers — without the jargon. All articles are grounded in official

U.S. data sources including the Federal Reserve (FRED), SEC filings,

and the Bureau of Labor Statistics.