Two Great Strategies, One Big Question

If you have a Roth IRA and you’re trying to figure out what to actually put inside it, you’ve probably come across two popular answers: a target date fund or a 3-fund portfolio. Both are solid, low-cost, index-based approaches. Both can help you build real wealth over time. So which one is right for you?

The honest answer: it depends on how hands-on you want to be. Here’s a side-by-side look at both strategies so you can make a confident call.

What Is a 3-Fund Portfolio?

The 3-fund portfolio is exactly what it sounds like — three index funds that together cover the entire investable market (source):

- A total US stock market fund — covers every publicly traded US company

- A total international stock fund — covers stocks outside the US

- A total bond market fund — adds stability and income

This approach was popularized by the Bogleheads, a community of investors who follow the philosophy of Jack Bogle, the founder of Vanguard Group (source). The idea is straightforward: own the whole market, keep costs razor-low, and stay the course.

In practice, a classic 3-fund Roth IRA might look like this:

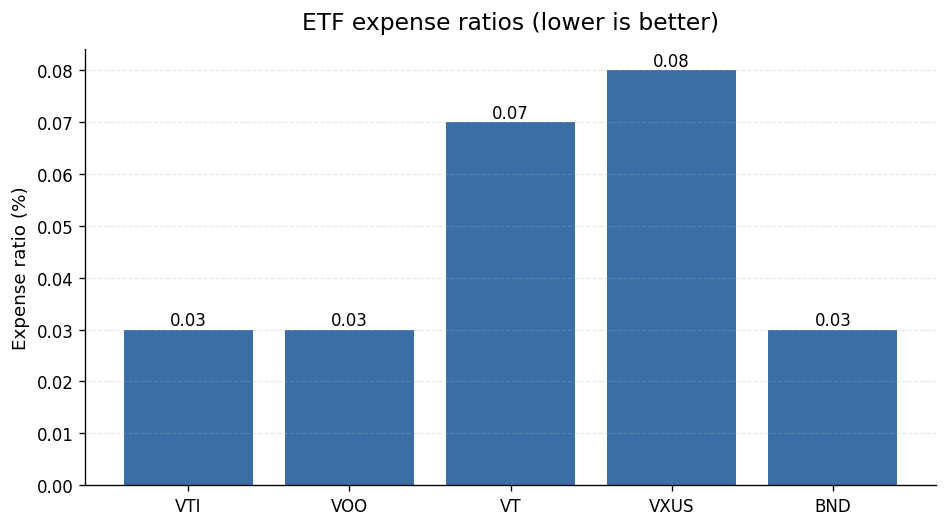

- VTI (Vanguard Total Stock Market ETF) — expense ratio of 0.03% (source)

- VXUS (Vanguard Total International Stock ETF) — expense ratio of 0.08% (source)

- BND (Vanguard Total Bond Market ETF) — expense ratio of 0.03% (source)

Those costs are remarkably low. On a $10,000 investment, a 0.03% expense ratio runs you just $3 a year.

Some investors swap VTI for VOO (Vanguard S&P 500 ETF), which also carries a 0.03% expense ratio (source), focusing only on large-cap US stocks rather than the full market.

Others simplify the international piece with VT (Vanguard Total World Stock ETF) at 0.07% (source), which bundles US and international stocks into one fund — making it more of a 2-fund approach when paired with BND.

What Is a Target Date Fund?

A target date fund is a single, all-in-one fund built around the year you plan to retire. You pick the fund closest to your expected retirement year — say, a 2055 fund if you plan to retire around that time — and the fund handles the rest.

Under the hood, most target date funds hold the same basic building blocks as a 3-fund portfolio: a mix of US stocks, international stocks, and bonds (source). The key difference is that the fund automatically adjusts its mix over time, gradually shifting toward a more conservative allocation as your target year approaches.

That automatic adjustment is the fund’s core selling point. You never have to log in and rebalance. You never have to decide whether to add more bonds as you age. The fund handles it for you.

Head-to-Head: Cost

Cost is where the 3-fund portfolio has a clear edge.

A DIY 3-fund portfolio built with Vanguard ETFs can run as cheap as 0.03%–0.08% per year depending on the funds you choose. VTI and BND each sit at 0.03% (source, source), while VXUS comes in at 0.08% (source).

Target date funds are still cheap compared to actively managed funds, but they carry a layer of management overhead on top of their underlying holdings. That pushes their expense ratios a bit higher than the individual ETFs inside them. Over a 30- or 40-year investing horizon, even small fee differences compound in a meaningful way.

If you’re cost-obsessed — and inside a Roth IRA, you have every reason to be, since every dollar saved on fees is a tax-free dollar that keeps growing — the 3-fund approach wins on price.

Head-to-Head: Simplicity

This is where target date funds win, and it’s not close.

With a target date fund, you make one decision: pick the fund with the year closest to your retirement. After that, you contribute regularly and the fund takes care of rebalancing and shifting your allocation over time. There’s nothing else to do.

With a 3-fund portfolio, you take on a few more responsibilities:

- You choose your allocation — how much goes to US stocks, international stocks, and bonds.

- You rebalance periodically — if US stocks surge and your allocation drifts, you need to bring it back in line.

- You adjust over time — as retirement gets closer, you’ll likely want to shift toward a more conservative mix.

None of these tasks are complicated, but they do require some attention. If you’d rather never think about your investments again, a target date fund is probably the better fit.

Head-to-Head: Control and Customization

The 3-fund portfolio shines here. You decide exactly how much international exposure you want. You set your bond allocation. You can tilt toward small-cap stocks, add a REIT fund, or make any other adjustment that fits your goals and risk tolerance.

Target date funds offer essentially zero customization. The fund manager decides the allocation, the glide path, and the underlying holdings. If the fund holds 20% international stocks and you’d prefer 30%, there’s no way to change that within the fund itself.

For investors who have thought carefully about their risk tolerance and want their portfolio to reflect those preferences, the 3-fund approach offers real flexibility.

Which One Is Better for a Roth IRA Specifically?

A Roth IRA is a tax-advantaged retirement account — and because both strategies work well inside one, the choice really comes down to your personal style.

Here’s a quick guide:

Choose a target date fund if you:

– Are just starting out and want the simplest possible setup

– Know you won’t rebalance on your own

– Prefer a “set it and forget it” approach

– Don’t want to research fund allocations

Choose a 3-fund portfolio if you:

– Want to minimize costs as much as possible

– Are comfortable doing an annual rebalance

– Want control over your US vs. international vs. bond split

– Enjoy being an active (but still passive!) participant in your investing

Both strategies are far better than leaving your Roth IRA in cash or picking individual stocks. The best portfolio is the one you’ll actually stick with.

A Note on the “One-Fund” Middle Ground

If the 3-fund portfolio sounds like too much work but you still want low costs, consider a single global ETF like VT (Vanguard Total World Stock ETF) at 0.07% (source). It skips bonds, so it’s not a full 3-fund portfolio, but it gives you instant global diversification in one ticker. Pair it with BND at 0.03% (source) and you have a 2-fund portfolio that’s nearly as simple as a target date fund — but cheaper.

Bottom Line

There’s no universally “better” choice between a target date fund and a 3-fund portfolio. Target date funds win on simplicity and automation. The 3-fund portfolio wins on cost and control. Both are excellent, evidence-based strategies built on the same core idea: own the market, keep fees low, and stay invested for the long haul (source).

If you’re just getting started, a target date fund is a perfectly smart choice. If you’re ready to take the wheel, the 3-fund portfolio gives you a powerful, low-cost engine to work with. Either way, the most important step is simply getting started.

This article was researched using official U.S. data sources cited inline and reviewed for accuracy before publishing. It is general information, not personalized financial advice. For decisions specific to your situation, consult a licensed professional.

Data refreshed: 2026-05-22. Editorial accuracy verified for cited sources only.

Armin Cole has been personally investing in index funds and ETFs

for over three years. He started Nestvestify to document what he’s

learning and make data-backed personal finance accessible to everyday

readers — without the jargon. All articles are grounded in official

U.S. data sources including the Federal Reserve (FRED), SEC filings,

and the Bureau of Labor Statistics.